Key Takeaways

- Money terms everyone should know include the fundamentals that shape everyday finances, such as checking and savings accounts, assets and liabilities, net worth (what you own minus what you owe), inflation, credit scores, APR (the cost of borrowing money), and APY (the interest your savings can earn).

- Understanding how credit works—including credit scores, credit reports, credit utilization, APR, and minimum payments—can directly impact your ability to borrow money and determine how much interest you pay over time.

- Knowing key tax concepts like tax brackets, deductions, and credits helps you understand how income is taxed and how certain actions can reduce what you owe or increase refunds.

- Building long-term wealth often comes from investing and retirement planning, including stocks, bonds, index funds, ETFs, 401(k)s, and IRAs, all of which benefit from compound interest to grow money over time.

Do you know the difference between APY and APR? Tax credit versus tax deduction? What about IRA and 401k? What does net worth actually mean? Schools didn’t teach you this stuff. Our parents probably forgot to. And banks, they hope you never learned.

And even though we deal with money every single day, only 50% of Americans are actually financially literate.1 So, consider this article your financial literacy crash course that will not only save you stress, but will save you real money. We’ll start with the basics and work our way up to the more complex terms.

Financial Literacy and Your Money

Financial literacy starts with storing your money in the right place. In recent years, mobile banking has skyrocketed in popularity with nearly half of banked households in America using it as the primary method of handling their financial accounts.2 A few perks of mobile banking include:

- Access your accounts 24/7

- Deposit checks by simply taking a picture with your smartphone

- Receive instant notifications on transactions (can help detect fraudulent activity quickly)

- Enhanced security with biometric logins, data encryption, etc.

- Digital wallet integration

Most mobile banking services come in the form of an app you can download on your smartphone or tablet. We recommend Current for mobile banking services. With Current, you can store money safely, get rewarded for saving, and even invest, so you can make the most of each and every paycheck.

Now let’s get started with our top 28 money terms everyone should know:

1. Checking Account

Your checking account is where your everyday money lives and your paycheck lands. Money moves in and out of this account nearly every day because you probably use it to buy things, pay bills, and swipe your card.

2. Savings Account

You also probably have a savings account, and it is exactly what it sounds like, a place where you save money and store it for later. You can only withdraw from a savings account a limited number of times per month before your bank actually charges you.

Savings accounts are considered a better place to store money because of interest, also known as yield. We’ll go over what these terms mean in a bit, but for now, just know that interest helps the money in your account grow.

3. High-Yield Savings Account (HYSA)

A high yield savings account is like a better savings account that pays you more interest, therefore helping your money grow faster. The interest is called APY, and it’s a percentage of your money in your account that you can earn.

For example, if your high yield savings account is 5% APY and you start the year at $1,000, you would have $1,500 at the end of the year.

HYSAs typically offer four to 5% APY, which is 10 times more compared to regular banking accounts. The reason they pay you is that all banks loan out your money to other people in businesses, and the banks charge an interest or a percentage of the loan. Banks usually keep most of this money, but HYSAs pay some of it to you.

4. Certificate of Deposit (CD)

A CD or certificate of deposit is like a savings account where you actually lock your money for a set time. And as a reward, the bank gives you a higher interest rate compared to a savings account, so you make more money.

It’s important to note that some interest rates with CDs are higher than regular savings accounts, but both options have yields that are lower than HYSAs, and more importantly, inflation.

If inflation is higher than your yield, you lose money over time. And it’s a big reason the millionaires and billionaires of the world invest the majority of their money in things like stocks and real estate instead of storing it in a savings account.

5. Overdraft

And then there’s overdraft, which you never really want to see because that means you spent more money than your account could cover. The bank usually covers it if you have overdraft protection, but they charge you a fee. So you want to avoid this when you can.

Okay, now that the basic warm-up is done, let’s talk about the other stuff every adult should know.

6. Assets

Next up, assets. These are things you own that are actually worth something. They can include:

- Cash

- Car (even if its old and rusty)

- Your house

- Investments

- Money in your savings

7. Liabilities

Liabilities are the opposite of assets. These are big things that you owe like:

- Credit cards

- Student loans

- Medical bills

Basically, anything that makes your money run dry.

8. Net Worth

When you take your total assets and subtract your liabilities, you get your net worth. This is basically your money scoreboard. It’s everything you own minus everything you owe.

If your assets go up and your liabilities go down, your net worth increases.

So, if you have 385K in assets like savings, your home, and investments, and 335K in liabilities like loans, and debt, your net worth is $50,000.

9. Depreciation

Depreciation, on the other hand, is not good. It’s a fancy word that basically just means something is losing value over time. Your phone is a great example. The minute a new one drops, your old one is basically a potato.

Your car is another example. As soon as you leave the car lot with a new car, it immediately starts losing value. Exactly why it’s a great idea to just buy used. And speaking of things losing value, let’s talk about inflation.

10. Inflation

Inflation is when prices go up and your money buys less. Cumulative inflation is up about 86% since the year 2000.3 Which means 10 years ago, $100 of groceries filled your entire cart. But today, $100 might get you three bags of groceries if you’re lucky. That’s inflation at work. Your dollar is shrinking while prices climb.

11. Tax Bracket

Next up, let’s talk about everyone’s favorite topic, taxes. I know what you’re thinking, but I promise I will make this painless. First, we’re talking tax brackets. Your tax bracket is basically the government saying, “Hey, you made this much, so here’s how much we’re taking.” And the more you earn, the higher the bracket you’re in. So, even though you’re leveling up in terms of income, the government is taking more money.

At the federal level for 2025, for a single person, the brackets start at 10% on taxable income up to $11,925. Moved to 12% for 11,926 to $48,475. Then 22% from $48,476 to $103,350. After that, there are higher brackets, 24%, 32% and 35% before you reach the top bracket of 37% for income over $626,350.4

12. Income Tax

On top of this, your state also taxes your income. And the income tax ranges from 4% for lower earners all the way up to 10% for higher earners, depending on your state. So, as your income goes up, you’re not just paying higher federal taxes, you’re paying state taxes, too, which means the government takes more of your money.

13. Tax Deduction

Tax deductions, however, lower the amount of income the government is actually allowed to tax you for. So, for example, if you paid student loans this year, you might be able to deduct $2,000 from your taxable income. So, if you owe $800 and get a $200 credit, you now owe $600.

Tax credits are basically the government rewarding you for doing certain things like having kids, paying for school, installing clean energy, having a moderate to low income, and so on.

14. Credit Score

All right, now that we’ve talked about taxes, let’s talk about something that affects almost every part of your life. Your credit. Your credit score is really your trust score with money and it can range from 300 to 850.

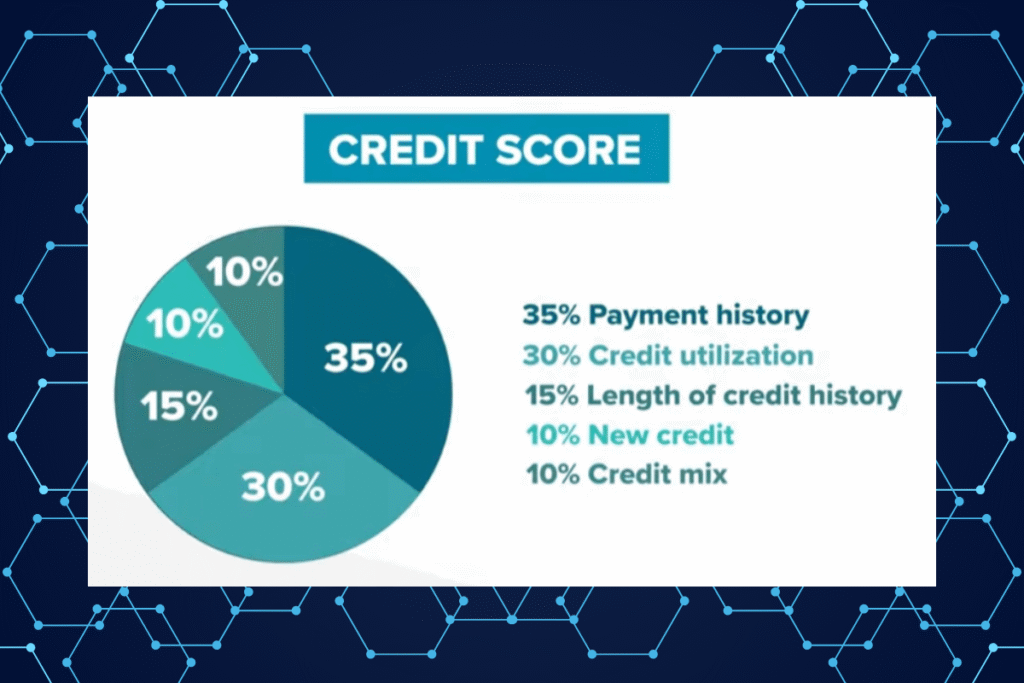

But if you have a low score, lenders treat you like they can trust you less. So they lend you less money or have super high interest rates. And here’s how that score is actually calculated.

- 35% Payment History — Do you pay your credit card bill on time?

- 30% Credit Utilization — How much of your total credit limit are you actually using? If your utilization goes above 30%, it starts to really hurt your credit score.

- 15% Length of Credit History — How long have you had credit accounts open?

- 10% New Credit — How often do you apply for new credit? Too many inquiries can hurt you.

- 10% Credit Mix — Having a variety of credit loans, credit cards, etc. helps your score.

So that three-digit number is really a mix of:

- Do you pay on time?

- How much debt are you carrying?

- How long have you been managing credit responsibly?

15. Credit Report

Now, your credit report is basically your full money story. This tracks everything, your loans, payments, debts, mistakes, all of it. And this is the thing landlords and lenders check before deciding to trust you. Some jobs even check into it to see how responsible you are. So, it’s something you should be on top of.

16. Total Credit

Total credit just means the maximum amount your credit card will let you borrow and it’s a huge part of your credit score. So if your credit card has a $1,000 credit line and you use 500, that’s 50% utilization. And basically keeping this utilization lower helps your credit score.

17. Minimum Payment

Now your minimum payment, this is just what it sounds like. It’s the minimum amount you have to pay towards your credit card bill. But only paying the minimum is kind of like paying rent on your debt. And rent never ends. So, it’s wise to pay more than the minimum towards your bill if you can.

18. Annual Percentage Rate (APR)

So, now you know the minimum payment, but here’s the real thing that could trap you if you don’t understand it. APR is how much a loan or credit costs you in a year. So, higher APR equals more money out of your pocket.

For example, if your credit card has 25% APR, that means you carry a balance. The credit card company is charging you 25% interest over a year on that amount. And you can find your APR listed right on your credit card statement, usually in the interest rate and fees section. You’ll also see it in the terms and disclosures when you first open the card.

Remember at the beginning when we mentioned APY and savings accounts? Well, APY is how much your savings earn in a year, including compound interest. Much nicer.

19. Personal Loan

Now, when life happens and emergencies pop up, which they do, you can get a personal loan. This lets you borrow money and pay it back over time with interest. A personal loan means you’re borrowing money as an individual, not as a business. You can get one from a bank, a credit union, or an online lender, and you pay it back over time with interest.

20. Emergency Loan

If you need help fast, there’s a type of personal loan called an emergency loan. Emergency loans are designed to be approved quickly, and you can qualify even if your credit score isn’t perfect.

So, if you need help in one of these moments, CreditNinja offers fast and simple personal loans so you’re not stuck waiting for money when you need it.

21. Stocks

So, we’ve talked about borrowing money, but let’s talk about growing money. We’re going to dive into the basics of investing. We’ve all heard about stocks, but few of us really understand them. Stocks are basically tiny pieces of a company you can own.

Some examples of top stocks people invest in are Apple, Netflix, and Google. If the company grows, your stock grows, too, and that’s great. Stocks can also go down if the company struggles or if the market dips.

22. Bonds

If you want something a little calmer than stocks, something that doesn’t bounce around as much, you can consider bonds. Bonds are basically IOU’s. When you buy a bond, you’re lending money to a company or the government. And when the bond’s time is up, they give you back the cost of your bond plus interest.

23. Index Funds

There are also index funds. Index funds are awesome because they give you a whole basket of different stocks, which makes investing way safer for beginners. And that basket is based on an index, which is just a list of companies that follow a certain part of the market.

For example, the S&P 500 is an index made up of 500 of the biggest companies in the US. So, if you’re a type who doesn’t want to pick the wrong stock, an index fund lets you invest in the whole group at once.

But if you want that same basket of stocks plus the freedom to buy or sell whenever you want during the day, that’s where ETFs come in.

24. Exchange Trade Fund (EFT)

An ETF or exchange trade fund looks like an index fund, but the key difference is that you can trade anytime the stock market is open.

25. 401k

Now, if you’re talking long-term investments like retirement, that’s where the next one comes in. A 401k. This is a retirement plan from your job. Every time you get paid, you can automatically take some of your paycheck and place it in this investment account. Your employer might even match some of your contributions, which is incredible because it’s free money.

Just remember, a 401k is meant for retirement, so you’re not supposed to take your money out until you’re 59 and a half. If you withdraw earlier, you usually are hit with a penalty fee in taxes. But if you want more control or your job doesn’t offer a 401k, then you should know about IRA.

26. Individual Retirement Account (IRA)

IRA are special retirement accounts that you can open yourself. A traditional IRA uses pre-tax income, which means you can deduct your contributions from your taxes now, and you’ll pay taxes later when you withdraw the money after age 59 and a half.

27. Roth IRA

A Roth IRA is the opposite. You put in post tax income, money you’ve already paid taxes on. So, when you withdraw after 59 and a half, you get your money tax-free because you already paid those taxes upfront.

When it comes to an IRA vs a Roth IRA, your future self will be very happy with either one. IRA’s are a great place to store your money, but really all retirement and investment accounts benefit from something called compound interest.

28. Compound Interest

Compound interest feels like a magic money trick, but here’s how it works. This is when your money earns money and then that money earns money and then suddenly your balance is growing faster than you ever expected. This is how normal people, not just rich people, actually build wealth.

A Final Word From CreditNinja

Now, all of this, credit, loans, investing, it all leads to one big truth. You don’t need to be some finance genius who’s perfect with money. But knowing these simple common money words will help you make better choices, dodge debt traps, save faster, and ultimately protect yourself and your wealth. When you understand money, money gets easier, and life does, too.

Sources:

1. Can you answer these 3 questions about your finances? The majority of US adults cannot | We Forum

2. FDIC Survey Finds 96 Percent of U.S. Households Were Banked in 2023 | FDIC

3. Inflation Calculator

4. 2025 Tax Brackets and Federal Income Tax Rates | Tax Foundation