Key Takeaways

- Money milestones you must hit in your 20s include aggressively paying down high-interest debt, building strong credit, and avoiding lifestyle choices that delay long-term financial stability.

- Eliminating credit cards, student loans, and unnecessary car debt early frees up cash flow, protects your credit score, and prevents interest from adding years to your working life.

- Finding and committing to a career path you can grow in increases earning potential over time and makes it easier to save, invest, and stay consistent financially.

- Budgeting, building 3–6 months of emergency savings, investing for retirement early, and preparing for major purchases like a home create compound advantages that carry into your 30s and beyond.

The clock is ticking in your 20s, and there are only six financial goals that truly matter to set yourself up for financial success by the time you’re 30. Skip even one of these and you can add 10 years to your working life.

Money Milestone #1: Pay Off As Much Debt as Possible

Your 20s are when most people either build up their financial future or ruin it. So, the first milestone to hit is to pay off as much debt as possible. And if you can pay all of it off, even better.

Your 20s are for paying off stuff like your credit card debt, student loan debt, and car loan debt if you have some, instead of taking on more.

In 2025, the average credit card debt for Gen Z is about $3,500, while millennials are nearly double that.3 So, if you can shrink your debt into your 20s, then you’re already getting ahead compared to others. Only 35% of consumers between 18 and 34 have paid off their credit cards in full.

If you aren’t paying your credit card debt in full, then you’re likely to fall into two categories:

- You can afford to pay it off, but you just aren’t.

- You can’t afford it at all.

And if you’re in the first category, then you’re making a big mistake. Why? Interest will eat you alive, especially when average credit card interest rates are around 26%.10 Now, if you’re in category 2, then watch these videos for how to pay off credit card debt fast.

The biggest form of debt that you’ll likely have in your 20s is going to be your student loan debt. Studies have shown that the average student loan borrower will pay $26,000 in interest alone over the life of their loan. Now, it varies state-to-state, but the average student loan debt for Americans under 30 is $23,795.1 But what really matters is how much money you’re making compared to how much money you owe. This is important now more than ever because one in three student loan borrowers are over 90 days past due, and this is at an all-time high record.11 But it’s important that you have a realistic plan.

Some experts suggest that your monthly payment should be at least 8 to 10% of your annual salary. So if you’re coming in out of school and making $30,000 a year, then your payment should be around $300. While $60,000 a year earners would pay more like $600. If 10% doesn’t feel manageable, then you’re probably paying either too much on other things like your car or where you live.

Which brings us to the next two big forms of debt that you have to pay off. In your 20s, you don’t need a fancy car. Because here’s the thing, the value only goes down the moment you drive it off the lot. Since you need to focus on paying off debt, every dollar that goes into that car is keeping you only in more debt. So, unless you’re very comfortable financially, chances are that you’re looking at used cars here.

Experts recommend keeping your car payment under 10% of your monthly take-home pay and avoiding loans that are longer than 5 years. So, take 10% of your salary and then multiply it by 60 monthly payments. And that should be close to what you’re looking at for your total car cost.In your 20s, you’ll also likely be living in an apartment for a bit. Your apartment should not be more than 30% of your gross income, which is the money that you make before taxes.

So, let’s say you make $60,000 a year. That’s $5,000 a month in gross income, which means that your apartment should be no more than $1,700. Again, this isn’t a firm rule, and it’s only a small piece of your financial puzzle.

Another reason why it is so important to pay off your debt early is that it will ultimately help you build up your credit score. Studies have shown that the average credit score for someone in their 20s is around 680 to 700, which is considered good.12 But as you get older, you’ll want to get into the high 700s as soon as possible to get the best rates possible. With a higher credit score, you can actually get approved for better loans that could save you tens, if not hundreds of thousands of dollars in your lifetime.

And speaking of apartment living, some people can actually skip that first and last month deposit that most apartments make you have as a down payment if you have a higher credit score.

Now, a key factor in your credit score is actually making payments on time. Just missing one of these payments for either your loan or your credit card could hurt your credit score for over 7 years.

Money Milestone #2: Find Your Career

Now, of course, we can’t pay off any of these forms of debt without income, right? Which brings me to financial milestone number two, finding your career. And no, we don’t mean just finding a job in your 20s. Finding a career field that challenges you, that you can also grow in, and that you actually enjoy will help you make even more money.

Now, the more experienced you are in your career, the higher your earnings potential. Work is always going to feel like work at some point. So, it’s important to build experience in something that you actually don’t hate and maybe enjoy for once. When you’re in your early 20s, you may not know what you want, but this is actually the best time to test out different industries. When you’re fresh out of school and you’re trying to build your skill set, you’re not going to be too picky when finding a job. And the job market is incredibly competitive thanks to AI and remote work, which means that you aren’t just competing locally for jobs, but you’re actually competing for one role with many people from around the country or around the globe here.

But regardless of the job market, you should choose your career sooner to increase your earnings potential. Job hopping is okay as long as you’re happier and ideally making more money each year. So, in that case, by all means, hop along. But remember, your 20s aren’t the time to settle. but a time to experiment and find a career that you’ll find fulfillment in. If you think that you want to go into marketing but end up hating it, try something else. But do not job hop just because it’s challenging and because you want to switch careers so that you’re essentially just starting from scratch every time. So, not only could you go from making 60, 70, or even 80K and then starting all over again, but if you are on the verge of getting a six-figure job in your current industry, it could be 5 to 10 years before you get another one. So, while job hopping is fine, career hopping is a whole other beast.

Money Milestones #3 and #4: Build a Budget and a Savings

And now, once you start making money, you need to work on milestones three and four, which are building a budget and a savings.

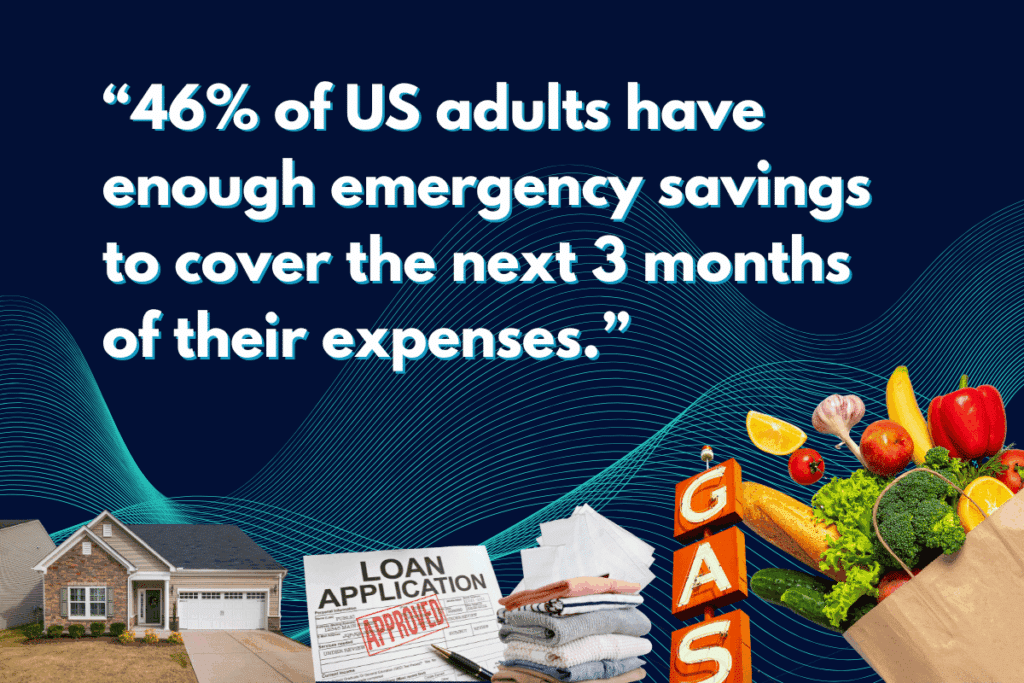

Look, we’re not going to sugarcoat it here, okay? It is pretty tough out there right now. Only 46% of US adults have enough emergency savings to cover the next 3 months of their expenses, according to Bank Rates’s 2025 emergency savings report.13 And only 31% of Gen Z-ers say that they even have enough savings to cover an unexpected $1,000 expense compared to 43% of millennials. For people under 35, the latest research shows that the medium amount of money in savings and checking accounts is $5,400.13 Not only are things even more expensive, but it feels so incredibly hard to save money because of how easy it is to spend it. And if this doesn’t scare you into finally budgeting and saving money, we don’t know what will. Now, either you make more money or you save more money. And in your 20s, you should be doing both.

To make more money, you can either get promoted, get raises, or job hop for a higher salary, or you can start a side hustle.

Exactly how much money do we need in our savings before we can start feeling comfortable? Is it $5,000, $10,000, or more? Well, the general rule of thumb here is that you should have about 3 to 6 months worth of expenses in your savings and checking accounts to cover any emergencies that you might have (let’s say you lose your job, have a medical emergency). This way, you’re covered while you search for another one or at least build back up anew. And the only way that you’ll know this number is by budgeting, knowing how much you have to spend and how much money you have left over each month.

If you have less than $5,000 in your bank account, then you should definitely watch our video right here on the next steps that you should take:

Money Milestone #5: Invest for Retirement

Once you get your emergency fund settled, some people actually prefer to be light on cash in their savings and checking accounts because they would rather invest. Which brings us to the fifth financial milestone, which is investing for retirement. And we get it, you’re not even thinking about getting old and retiring, right? Well, for Americans under 35, the average amount saved in their retirement account is just under $50,000, while the median is just under 20,000.8 But believe it or not, right now is the time when retirement investing is so important because it’s going to have the biggest impact because of two words, compound interest. So that’s why you should try to start investing even if it’s in really small amounts at times.

Let’s compare two scenarios here where you start investing when you’re 20 versus when you start investing at 30. In the first scenario, let’s say you started investing $100 every month at 20 until you hit the age of retirement at 65. At retirement, you’d have $463,000. But if you waited to start investing at the age of 30, you would only have around $200,000. That means that in the first scenario, you would have made an extra quarter million just by investing 10 years earlier, and it only cost $12,000 more.

In both scenarios, you can see that the growth doesn’t really add up that fast. But later on in life, the savings go ballistic. So the sooner that you can start investing, the sooner you can benefit from compound interest.

The two most common ways to contribute to your retirement are going to be auto-deducting that directly from your paycheck into your account. Or if you take whatever leftover money that you might have from your cash flow and savings and then just manually contribute it there. But now if you have an employee 401k then they might offer what’s called an employer match. They’ll actually match some of that salary that you put into retirement up to a certain amount. So if you put in, let’s say, $200 from your paycheck towards retirement, your job might put in $150. It’s basically free money. But regardless of whether your job sponsors a retirement account, you should open up a Roth IRA where your money can grow tax-free for the rest of your life. Even without that 401k match from those former employers, you can still have a Roth IRA to contribute to monthly.

Money Milestone #6: Prepare for Big Purchases

The sixth milestone for your 20s is to prepare for the inevitable big purchases coming in your 30s, or earlier if you play your cards right. About one in three people under 30 actually own a home. And the median age for that first time home buyer is going up and up because people are owning homes later in life due to rising costs.

Now, we can’t predict what’s going to happen in the housing market with prices either rising or falling. But no matter what, you really need to start preparing as if this is something you want to do. If you’re in your early 20s and you want to buy a house, you have an advantage because you have more time to prepare for that rising housing cost. People in their late 20s and 30s could have never expected the years of COVID and what that did to the housing market. Home prices spiked massively in such a short amount of time and it left most people unable to afford a home. But you have a lot more time to prepare if you are in your 20s to start investing now so that you can enjoy later.

The first step to owning a home is getting a good or great credit score. Like we talked about earlier, right now the medium home price is $415,000.9 So if we can lower our interest rate by even just a half percent, we could save tens of thousands of dollars. So please, for your own sake, don’t ignore your credit score. Building credit is adulting.

Regardless of how much money you make or how expensive that house is, the fact is your down payment will probably be in the five to six figures. So, if you can start saving even just a little bit every month in a high interest savings account, you will be well on your way to affording that home when it comes to making that down payment.

Now, if you don’t have a high interest savings account, then watch this video right here.

And if you want to buy a house, then watch this one right here.

Sources:

- Average Student Loan Debt by Age [2025]: Facts & Statistics | Educational Data

- How Much College Debt is Too Much? | University of Florida

- Average Credit Card Debt Increases 3.5% to $6,730 in 2024 | Experian

- Average Time to Repay Student Loans | Educational Data

- Here’s the average student loan debt of borrowers 35 to 49 years old | CNBC

- The Fed – Table: Survey of Consumer Finances, 1989 – 2022 | Federal Reserve

- What Is the Average Savings Account Balance? | SmartAsset

- Average Retirement Savings by Age | NerdWallet

- US Existing Home Median Sales Price (Monthly) | United States

- Average Credit Card Interest Rate for August 2025: 23.99% APR | Investopedia

- One in three student loan borrowers risk default as delinquency rates soar | Congress.gov

- Credit Score by Age: What to Aim for in Your 20s, 30s & Beyond | Ally

- Bankrate’s 2026 Emergency Savings Report