Key Takeaways

- Almost 46% of American households carry credit card debt, highlighting that nearly half of U.S. consumers rely on revolving credit.

- Middle-income, working-age families hold the largest total balances, while low-income and minority households bear the heaviest debt relative to income.

- Families with children, renters, and metro-area residents tend to carry larger balances than childless or rural households.

- High average interest rates make even small balances expensive, and missed credit card payments can quickly escalate debt.

About 46% of Americans carry credit card debt, according to the Federal Reserve Bank. Rising credit card interest rates have made balances more expensive to carry, causing many households to fall behind on their required credit card payments. That creates pressure on monthly budgets and complicates debt repayment plans, especially when only minimum payments are made.

Understanding how interest rates and credit card interest compound on unpaid balances is essential for anyone trying to pay down debt and regain financial stability.

What Is Credit Card Debt?

Credit card debt is the unpaid credit card balance that credit cardholders carry from month to month when they cannot pay in full. According to the Federal Reserve Bank, this form of debt has grown as credit card interest rates rise, making credit card payments harder to manage.

Unlike personal loans, credit card balances often come with higher interest rates, leading to long-term debt repayment struggles. In personal finance, the credit card debt spread shows how borrowing affects monthly income and household stability.

What Is the Average Credit Card Interest Rate by State?

| State | Average credit-card balance (per user) | Estimated annual interest (21.16% APR) |

| Alabama | $6,619 | $1,401.42 |

| Arizona | $7,769 | $1,643.77 |

| Arkansas | $6,104 | $1,291.47 |

| California | $8,559 | $1,810.66 |

| Colorado | $7,322 | $1,549.62 |

| Connecticut | $8,416 | $1,781.28 |

| Delaware | $7,474 | $1,582.73 |

| Florida | $8,637 | $1,827.59 |

| Georgia | $8,663 | $1,833.09 |

| Hawaii | $7,883 | $1,668.97 |

| Idaho | $7,275 | $1,540.26 |

| Illinois | $7,141 | $1,511.86 |

| Indiana | $6,161 | $1,303.37 |

| Iowa | $5,795 | $1,226.49 |

| Kansas | $6,631 | $1,403.56 |

| Kentucky | $5,908 | $1,250.96 |

| Louisiana | $7,015 | $1,484.12 |

| Maine | $7,139 | $1,511.86 |

| Maryland | $9,047 | $1,914.35 |

| Massachusetts | $7,872 | $1,665.49 |

| Michigan | $7,016 | $1,484.38 |

| Minnesota | $6,989 | $1,478.16 |

| Mississippi | $6,146 | $1,300.76 |

| Missouri | $6,599 | $1,396.35 |

| Montana | $6,891 | $1,458.14 |

| Nebraska | $6,479 | $1,371.35 |

| Nevada | $8,378 | $1,772.78 |

| New Hampshire | $7,427 | $1,571.64 |

| New Jersey | $8,803 | $1,862.71 |

| New Mexico | $6,753 | $1,429.15 |

| New York | $8,920 | $1,887.47 |

| North Carolina | $7,487 | $1,584.96 |

| North Dakota | $7,163 | $1,516.04 |

| Ohio | $6,291 | $1,331.91 |

| Oklahoma | $6,601 | $1,396.99 |

| Oregon | $7,265 | $1,537.33 |

| Pennsylvania | $7,275 | $1,540.26 |

| Rhode Island | $7,494 | $1,586.18 |

| South Carolina | $7,388 | $1,562.12 |

| South Dakota | $6,332 | $1,339.86 |

| Tennessee | $6,843 | $1,448.79 |

| Texas | $8,186 | $1,732.29 |

| Utah | $7,991 | $1,691.55 |

| Vermont | $7,484 | $1,582.49 |

| Virginia | $8,353 | $1,767.02 |

| Washington | $8,364 | $1,769.26 |

| West Virginia | $5,938 | $1,256.68 |

| Wisconsin | $6,279 | $1,328.29 |

| Wyoming | $7,636 | $1,616.07 |

Why Do So Many Americans Carry Credit Card Debt?

Many Americans carry debt because wages and annual incomes have stagnated while living costs and unexpected expenses have risen. That combination, plus limited emergency savings and easy access to credit, forces households to rely on borrowing for everyday needs and emergencies.

High credit card interest rates and rising interest rates overall make balances harder to pay down, resulting in higher credit card delinquencies, turning short-term credit into long-term repayment burdens.

Most credit card debt comes from the result of the following:

- Stagnant wages vs. rising living costs and high inflation of everyday expenses

- Limited emergency savings / unexpected medical bills

- High credit card interest rates and fees

- Easy access to credit and reliance on minimum payments

- Student loans, housing costs, and job instability

These issues further amplify the problem, leaving many struggling to eliminate credit card balances despite steady employment.

What Is the Impact of Credit Card Debt in 2025?

The impact of credit card debt is that it raises borrowing costs, reduces spending power, and can push households into financial distress. Because an average interest rate is often high, cardholders end up paying more money over time for everyday retail purchases or emergency needs like car and home repairs.

That pressure can mean more than half of discretionary income gets redirected to interest and fees, increasing the risk of missed payments and making it harder to afford basics or make steady progress on debt repayment.

- At a Glance: Making only minimum payments can turn a small credit card balance into decades of repayment and many times the original amount in interest. Increasing your monthly payment even modestly greatly shortens payoff time and slashes total interest paid.

Which Demographics Are Most Affected by Credit Card Debt?

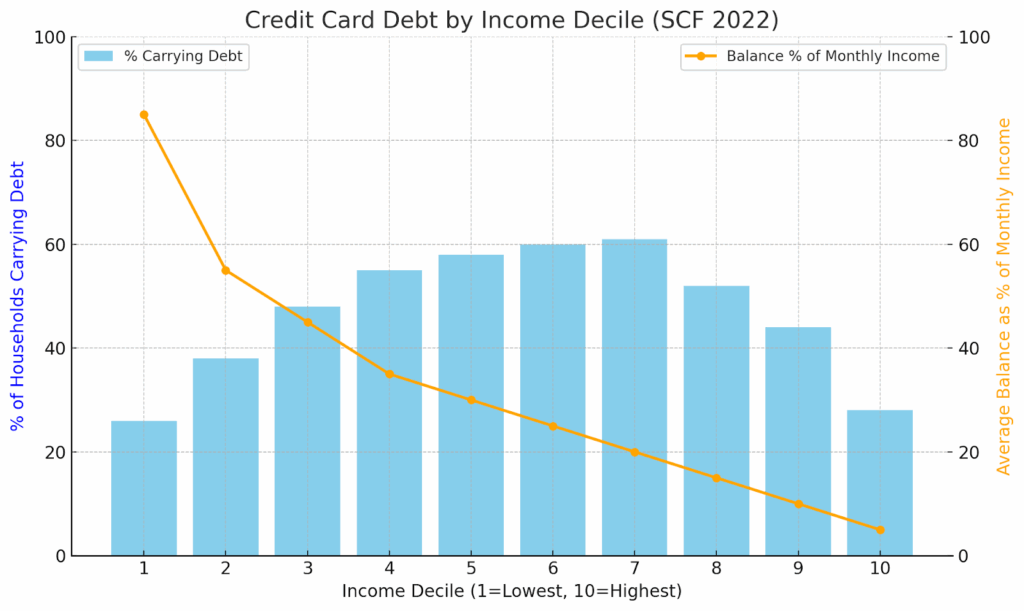

Credit card debt affects different households in different ways, but middle-income, working-age families typically carry the largest total balances. Low-income, minority, and renter households often feel the heaviest burden relative to their income. Here’s a closer look:

- Income: Households in the middle-income range (5th–7th deciles) are most likely to carry debt (~58–61%). The poorest and wealthiest households are less likely to have balances, but when low-income families do, their debt is a much larger portion of their monthly income.

- Age & Race: Younger adults carry balances more often than seniors. Black and Hispanic cardholders typically revolve balances at higher rates than White and Asian cardholders, increasing repayment challenges.

- Household Type: Families with children and married couples tend to carry larger balances (~$3,400 median) than childless or older households. Single adults under 55 also frequently carry debt.

- Renters vs. Homeowners / Region: Renters are more likely to carry debt than homeowners (56% vs. 47%). Metro-area adults hold higher balances (~$5,040) than rural adults (~$3,334), and housing costs amplify repayment pressure.

What Are Some Good Debt Repayment Strategies?

For many American households, managing credit card debt can feel like a slippery slope, but effective strategies can help consumers pay down balances while saving money. Popular debt repayment methods include the avalanche approach, which targets high-interest debts first, and the snowball method, which focuses on smaller balances to build momentum.

Other options include balance transfers or consolidation loans to lower interest costs. Building strong habits like paying on time, budgeting, and adjusting payments after a new job or changes in mortgage obligations helps households regain control and reduce financial stress.

FAQ

What percentage of Americans currently have credit card debt?

About 46% of American households carry credit card debt, according to the Federal Reserve Bank. Debt levels vary by income, age, and household type.

Who is most affected by credit card debt?

Middle-income, working-age families typically carry the largest balances, while low-income, minority, and renter households often feel the heaviest burden relative to income.

How do credit card interest rates impact repayment?

High average interest rates make credit card balances grow quickly. Even small unpaid balances can accumulate substantial interest if monthly payments are low.

What are the best strategies to pay off credit card debt?

Popular approaches include the avalanche method (pay high-interest cards first), the snowball method (pay small balances first), balance transfers, consolidation loans, and building consistent payment habits.

Can carrying credit card debt affect other financial goals?

Yes. High monthly credit card payments can limit savings, delay a mortgage, reduce flexibility for emergencies like car or home repairs, and increase financial stress.

References:

- Which U.S. Households Have Credit Card Debt? │ St. Louis Federal Reserve

- Consumer Loans │ St. Louis Federal Reserve

- Center for Microeconomic Data │ New York Fed

- Credit Card Banking │ New York Fed

- Consumer Credit – G.19 │ Federal Reserve

- Federal Student Loan Portfolio │Federal Student Aid

- Household Income Inflation │The Washington Post

- Wage Stagnation in Nine Charts │ Economic Policy Institute

- Making Ends Meet in 2022 │ Consumer Financial Protection Bureau

- American Renters and Financial Fragility │ FINRA

- Are Rising Rents Raising Consumer Debt and Delinquency?│ Federal Reserve Bank of Philadelphia