Key Takeaways

- Rent keeps going up because post-pandemic demand surged while housing supply stayed tight, mortgage rates and home prices priced millions out of buying, and housing inflation lags behind the rest of the economy, keeping rents elevated even when other costs cool off.

- Rents jumped over 30% between 2021 and 2023 due to a sudden return to renting after lockdowns, creating intense competition for limited units, and those increases never reversed.1

- Higher mortgage rates and home prices have trapped more people in the rental market for longer, increasing demand year after year without a matching increase in affordable housing supply.

- Landlords continue raising rent to offset rising costs like construction expenses, property taxes, insurance, and fees, passing those increases directly onto renters while income growth fails to keep pace.

Rent keeps going up, and there’s no end in sight. But is this due to the economy, greedy landlords, or is it because of the brutal housing market?

In this guide, we’ll break down why rent won’t stop going up and what you can do about it.

The Cost of Living Crisis Explained

Let’s start with the moment everything changed. Because once you see what shifted over the last few years, you’ll understand why rent never really came back down. After COVID, between 2021 and 2023, rent didn’t just rise, it jumped by over 30%.1

Let’s put that in perspective. If you were paying $1,500 a month in 2021, that same apartment costs you $1,950 today, that’s an extra $450 every single month or $5,400 a year.

Why did this happen? Because after lockdowns eased and people returned to normal life, they started renting again. But the supply couldn’t meet the intense demand, so rent prices soared.

And here’s what catches everyone off guard. Even when inflation calmed down following the post-pandemic spike, rent didn’t. That’s because housing inflation typically lags behind other inflation. So, while groceries and gas costs settle down, it takes rent much longer to reset.

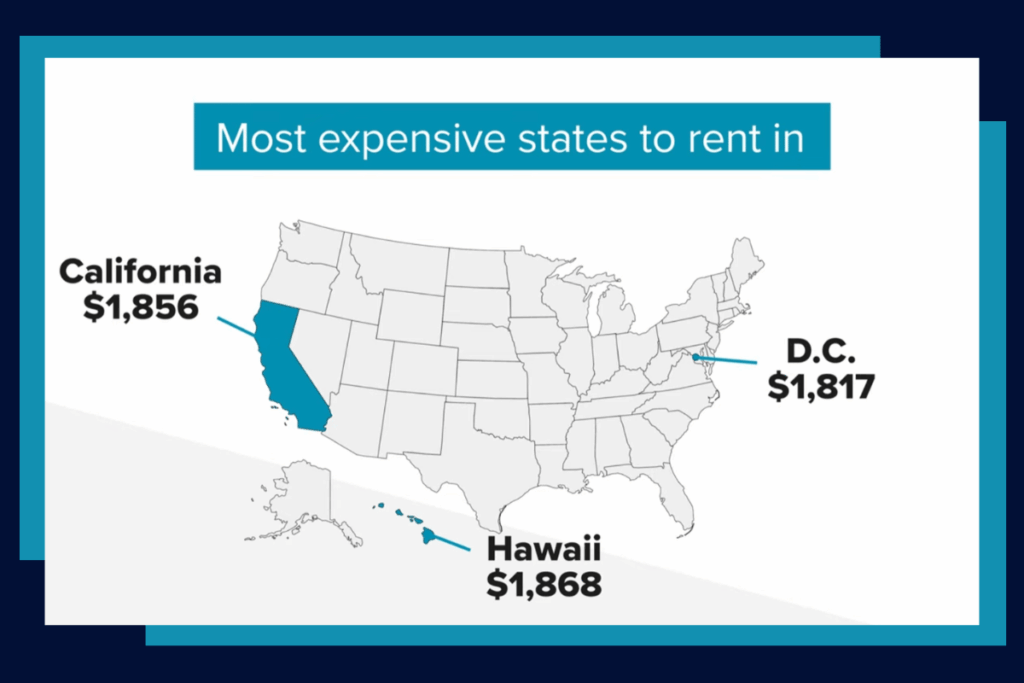

Today, the most expensive places to rent include California, Hawaii, and DC, with the median rent being around $1,600 to $1,900.2 For the least expensive states to rent in, we have West Virginia, Arkansas, and South Dakota, where medium rent is under $1,000.2 But regardless of where you live, the question is, can your income keep up with rising rent costs?

Income vs. Rent Prices Over Time

For decades, the path was simple. Rent for a few years, save up, buy a house. Your parents probably did it. Your grandparents definitely did. That was the ladder everyone climbed. But recently, something happened to knock millions of people off the ladder. The culprit, mortgage rates doubled from 3% to 6% in less than 2 years. And at the same time, housing prices surged.

Here’s what that means. A $400,000 home that would have cost you $1,700 a month in 2020, that same house now costs you $2,400 a month with the higher rate and higher price. That’s a $700 a month increase, which prices out millions of buyers. As a result, millions of Americans got trapped in the renting market. More renters all competing for the same units for longer periods of time. More demand, same supply. You know what happens next? Higher prices. You’ve probably noticed this, too. New apartment buildings are popping up everywhere. Cities, suburbs, doesn’t matter. So, one would think that there’s enough space available to see rent prices start to go down, right? But more buildings don’t automatically mean lower rent. And this is where things get counterintuitive.

Luxury Apartments vs. Affordable Housing

Now, let’s tackle the uncomfortable question everyone’s thinking. Why is there more luxury housing and not more affordable housing? Is it because landlords are just greedy? Of course, landlords and builders want to make more money, but they’re raising rents for two main reasons:

- Building costs have gone up with inflation.

Building is far more expensive for these developers than it used to be. So, they priced these luxury units higher from day one in hopes of making their money back ASAP.

- Costs for landlords have also gone up.

Property taxes in most states have skyrocketed, especially in places like New Jersey, Illinois, and Connecticut, where property taxes are already high, and they’re only continuing to climb.3 Colorado, Georgia, and Florida have seen some of the biggest property tax hikes in recent years, with Colorado seeing an increase of 10.6%.4 Insurance costs in places like Florida and Texas have also surged. We’re talking about a 75% increase in just a few years.5 And guess what? That entire increase gets passed straight to you.

Here’s an example of landlords passing costs on to tenants in New York City. Most rentals are done through real estate agents due to intense competition. They just passed a ruling in 2025 which requires landlords to pay a rental broker fee.6 This was something that used to be paid by the renter. So many units saw a 5.3% increase just to cover that fee.7 And here’s the hard truth. Rent is never going down. It’s going to continue to rise.

So when these increases hit, and they will, you need to be ready. That means having a financial cushion for emergencies. Too many people can’t cover a $1,000 emergency and resort to payday loans, which leads tons of people into cycles of debt. Other loan providers like CreditNinja offer emergency personal loans up to $5,000 that are typically delivered either the same day or the next business day. Watch this video to learn more.

How To Improve Your Renting Situation

But beyond having that safety net, there are actual tactics that you can use to fight back when your rent increase notice comes. Let’s break down how that works.

Negotiate Rent

First of all, the best time to negotiate rent is right after you get the notice about your rate.

Here’s what landlords know. Good tenants are valuable and turnover is more expensive for them, so they’d rather avoid it.

Before negotiating, make sure you do your market research about similar rental units in the area. If the new proposed rate is over market value, that’s leverage for you to ask for a decrease in your negotiation.

Highlight Your Value as a Renter

You’ll also want to highlight your value. Have you always paid rent on time? Are you a long-term, low-maintenance tenant? Do you have excellent credit? If that doesn’t work, try making a smart counter offer. Instead of just asking for a lower rate, ask for a longer lease, waved fees, and maybe even negotiate some amenities like free parking or a waved trash removal fee. Whatever it is that you’d like to secure, this is your time to mention it.

Use Your Knowledge as Leverage

Here’s what we know now. Rent didn’t break by accident. This isn’t just the market. It’s a perfect storm of policy failures, construction barriers, and costs getting passed down to the people with the least power to push back: renters. And yes, that’s infuriating because you’re doing everything right. You pay on time. You don’t trash the place. You’re a dream tenant. And your reward? $100 increases year after year for the same exact apartment.

The system is rigged against renters. Landlords can raise rates because they know you don’t have anywhere else to go. Builders won’t make affordable housing because luxury units are more profitable. And every cost increase, property taxes, insurance, broker fees, gets passed straight to you.

But here’s the thing, understanding the system doesn’t fix it, but it does give you leverage. You can’t change supply and demand, but you can negotiate from a position of knowledge. You can prepare financially so you’re not one emergency away from disaster. And you can make moves that protect yourself even in a rigged game.

So, don’t sit back hoping rent magically gets cheaper. It won’t. Instead, use what you know to fight back. Negotiate harder. Build that emergency fund and make choices that put you in control, not your landlord.

We published a series of videos on building wealth in your 20s, 30s, and 40s. Because the best revenge against the system designed to keep you renting forever, actually building enough wealth to escape it. Check them out below:

- 6 Financial Goals to Hit in Your 20s to Build Wealth & Financial Freedom

- 5 Financial Goals You Need to Hit Before 40 to Build Wealth & Financial Freedom

- 5 Financial Goals to Hit in Your 40s

Sources:

- U.S. Cities With the Biggest Change in Rent Prices | Construction Coverage

- The 5 Most (and Least) Expensive States and Cities for Renters | Earnest

- Tax Foundation: NJ Property Taxes Still Rank Highest | NJBIA

- Property Taxes Surging In Once-Affordable States | National Mortgage Professional

- The Fed – Rising Property Insurance Costs and Pass-Through to Rents for Apartment Buildings | Federal Reserve

- NYC’s FARE Act Resulting in ‘More Dynamic’ Rental Market | Globest

- City’s Anti-Broker Fee Law Kicks In for Tenants | The City