Key Takeaways

- Financial goals for your 40s center on building stability and resilience by increasing your emergency fund to 6–12 months of expenses, prioritizing saving over spending to protect against job loss, medical costs, and rising living expenses.

- Eliminating bad debt should be a top priority, with the goal of paying off credit cards, car loans, and student loans while maintaining only value-building debt and achieving a strong credit score through consistent, on-time payments.

- Retirement savings should accelerate significantly, aiming to have roughly six times your annual salary saved by age 50 by maximizing retirement contributions, investing consistently, and taking advantage of higher earning years.

- Long-term planning becomes essential, including diversifying income streams, preparing for healthcare and long-term care needs, securing appropriate insurance, and balancing future security with intentional spending on health, experiences, and family.

You’re full-on adulting in your 40s, and if you don’t have your finances together, you could be one doctor’s visit or flooded basement away from financial ruin. But good news, you’re reading this article, which means it’s not too late. So, if you want to enjoy the rest of your life, pay attention to the five financial goals and milestones you should hit in your 40s.

Financial Goal #1: Build a Bigger Emergency Fund

The first financial milestone for your 40s is building a bigger emergency fund. In your 30s, your emergency fund was 3 to 6 months of expenses. But in your 40s, you need at least 6 to 12 months in your emergency fund. Here’s why. Your 40s are your prime earning years. And it’s also when you’re spending more. You have more responsibilities like kids, potentially a home you own, and aging parents to take care of. And if your son breaks an arm, your mother-in-law breaks a hip, or the washing machine breaks, it shouldn’t break the bank to cover for the expenses.

Oh, and yes, inflation is raging. So everything is getting more and more expensive. So how much should you save? Let’s first look at income. According to 2025 data from the US Bureau of Labor Statistics, the median income for people 35 to 44 is around $72.020.1

For people 45 to 54, that grows to around $71,552. In 2025, 6 months of emergency expenses equals about 40% of the average American annual household income, which equals around $35,000.1

Let’s break this down. With layoffs happening left and right, you need to plan for emergency medical coverage in case you lose your job. So $11,635 of the $35,000 is the average cost of single coverage COBRA premiums multiplied by the average household. The next part of the $35,000 is for your car and that comes out to $10,621. This number is the average cost to own two vehicles and operate one.

Now, you also need emergency funds set aside for housing costs, which is recommended to be $9,785. This number is the average cost of housing and utilities for renters and homeowners.

And the final part of that $35,000 is $3,176 for food. This number is the average cost for 6 months of groceries. For many of us, 6 months of housing is a lot more than $9,785. So, that’s why you need to up your emergency savings even more just in case.

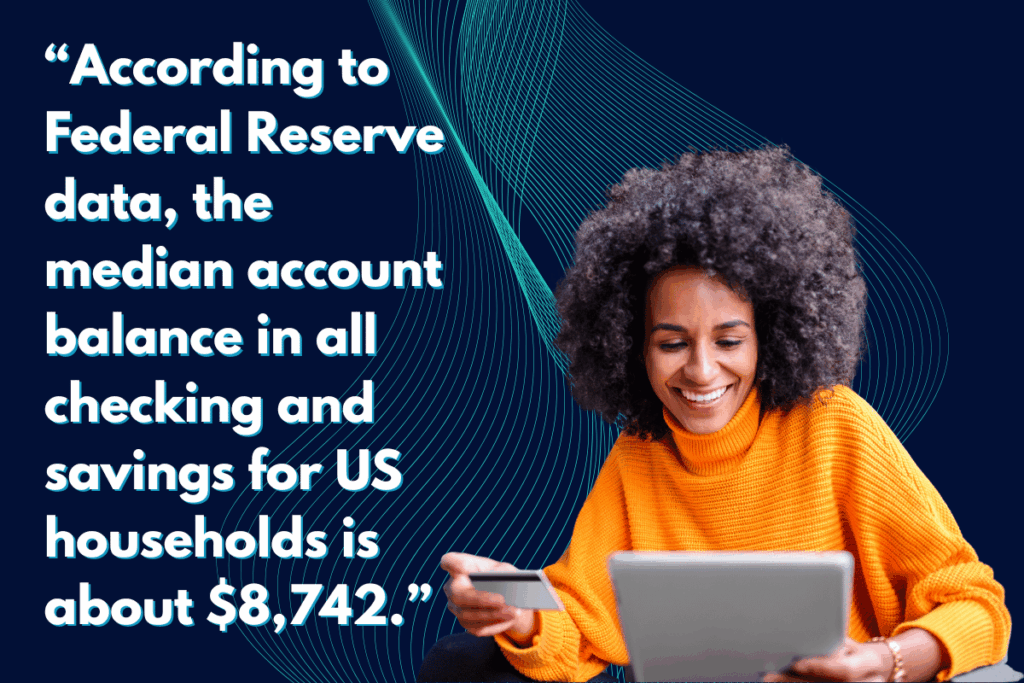

But here’s the kicker. According to Federal Reserve data, the median account balance in all checking and savings for US households was only about $8,742, which is only enough to cover about a month and a half of expenses for the average American household.2

So, if this is you, earning more and saving more needs to be your top priority. Have a yard sale. Ask for a raise. Drive Uber when you can. Whatever it is, you need to save more.

In your 40s, you should build good financial habits like having your emergency fund growing in a high yield savings account. So, at least the interest payments make up for some of the inflation. And if you’re extra on top of it, maybe you have additional savings growing in a short-term CD earning even more interest. But a sign that you’re in a good place is if there is a financial emergency, you don’t need to pull money out of your investments and pay tax or early withdrawal penalties.

If you’re reading this and thinking, “Well, that’s not me.” Don’t worry. This is the time that you can do the most to catch up, and we’ll tell you how. But no matter what happens, please never, ever, ever resort to a predatory payday loan that is made to trap you in more debt. In these cases where you need cash fast, tap into your emergency fund. And if you don’t have enough yet, get an emergency personal loan from a trusted provider like CreditNinja.

Financial Goal #2: Get Rid of Bad Debt

The next financial milestone to hit in your 40s is being free of all bad debt. Only holding good debt and building a high credit score. This also means you should have a high 700s or 800 credit score in your 40s because you’ve had two decades to build it.

But here’s an alarming stat. Americans aged 40 to 49 currently hold the most credit card debt of any age group.3 Gen X also has the highest car loans at $27,128 and second highest mortgage loans at $283,677.4 So, if you’re in this boat, it’s time to make some changes by eliminating bad debt.

Bad debt is any debt on things that don’t appreciate in value, like credit card debt, car loans, and those sneaky buy now pay later apps. Good debt, on the other hand, is like your home mortgage because your home appreciates in value over time.

In your 40s, you should have paid off all student loans, car loans, and make enough money to pay off your credit card statement in full and on time every single month. If you do all this, your credit score should be around the 800s. And that’s the goal. If it’s not there yet, definitely watch our videos on growing your credit score and paying off debt:

If you still have bad debt, pay it off as soon as possible. Because the real cost of debt isn’t just what you pay and what it does to your credit score, it’s that your money isn’t working for you.

Here’s an example that shows you how focusing on paying off bad debt like car loans now in your 40s can dramatically impact your future. Let’s say you have a car payment for $400 for 36 months, 3 years. Let’s not even include interest on your car loan for simplicity sake. $400 a month for 3 years is $14,400. Let’s say you’ve had enough saved to pay it off in full. Now, let’s say you invested that amount, $400 a month for 3 years, and let it grow for 20 years at 10% a year in the stock market. By the time you’re in your 60s, you would have $69,984. That is $55,584 more essentially free money that you wouldn’t have.

We know paying in full isn’t something most of us can do, but we just wanted to make sure you see how valuable it is to pay off bad debt as fast as possible so you can put more money into retirement.

Financial Goal #3: Save Six Times Your Annual Salary by Age 50

The next major milestone in your 40s is to have six times your annual salary saved for retirement by 50. We know this might sound like a lot, but if you do this in your 40s, you’ll have 10 times your annual salary by the time you retire. The exact number depends on where you live and your lifestyle.

Here’s an example. If you earn $80,000 a year, you should have $480,000 saved in retirement and investment accounts by the time you turn 50. And by the time you turn 67 and retire, just with a modest 7% of returns, your account will grow to more than 1.6 million.

Remember, the earlier you contribute, the more it can grow. If you’re feeling behind right now, you can still catch up. Make a plan to make as much income as possible, reduce expenses, and make hitting these money milestones the top priority.

Also, most people don’t know this, but the IRS lets you contribute even more in your 50s. $7,000 more in your 401k for a total of $30,000 a year and $1,000 more in your Roth IRA for a total of $8,500.

There’s also something called the SE IRA for those who are self-employed where you can contribute up to $69,000 a year or 25% of your annual income. And if you’re an overachiever and have maxed everything out, that’s when you can contribute to a regular brokerage and invest your money there.

Maxing out your retirement contributions also helps you optimize your taxes because the amount you contribute gets deducted from the income that you owe taxes on. Definitely work with a tax professional, but this is something else to consider since you’re likely making more income in your 40s.

One of the best ways to save and invest as much as possible now is to develop multiple income streams in your 40s, which means you’re not just relying on your day job. The economy is rough right now and layoffs are happening left and right, which means this is the decade for adding another income. If you have a great credit score, you qualify for a great mortgage and can buy a rental property to give you some extra income. Or since you’re experienced in your career, consider consulting on the side. Or take extra time to learn more about investing and invest in dividend stocks that pay out extra income. That all adds up

Financial Goal #4: Think About Long-Term Care

Not to be a downer, but in your 40s, you have to start planning your long-term care and your family estate planning. Did you know that around 70% of people over 65 will need some form of long-term care?5 And that ain’t cheap. The average nursing home costs around $7,000 a month. And while we hope our kids will take care of us, you just never know.

And we can’t really count on Medicare or health insurance to cover all the costs of long-term care. So to be safe, plan for it now. This is why you’re putting so much money and effort into investing for retirement.

Also, your 40s are the time to secure any life insurance or long-term care insurance because you have to get them now while you’re healthy. These companies won’t insure you when you need it. It’s like getting home insurance after your house floods.

And we know this is a financial goals article, but your 40s are the time to develop healthy habits like working out, lifting weights, and eating well. The healthier you are now, the less likely you’ll need early healthcare and long-term care. Your 40s are also for enjoying life. After all, you’ve worked so hard for decades already.

Financial Goal #5: Practice Intentional Spending

And in addition to planning for your future, you need to enjoy the present. If you’re feeling behind in your goals, yes, definitely make savings and investing a priority, but also intentionally spend.

Maybe you don’t need to upgrade your car or home and instead take a family road trip where your memories together are priceless. Studies show that experiences bring more happiness than things. Instead of buying Keeping Up with the Joneses, spend on quality food, health, and fitness that could give years back to your life.

Bonus Goal: Open a 529 Account

Here’s one bonus goal. If you have kids and you’re on your way to hitting your other 40s money milestones, consider opening a 529 account where you can contribute money for your kids education fund for college or graduate school.

We know we covered a lot in this article, but you’re already ahead of most people simply by reading through! Remember, your financial future is in your hands. And no matter where you’re starting from, the best time to start is right now!

Sources:

- The Average Salary by Age in the U.S. | Smart Asset

- The average savings account balance in the US: Here’s how much Americans have in the bank – Philomath News

- Which age group holds the most credit card debt in the US? | 4029tv

- Average Car Payment and Auto Loan Statistics: 2025 | LendingTree

- Most aging Americans will need long-term care in their lifetime. Loved ones often take on the labor and costs. – CBS News