Key Takeaways

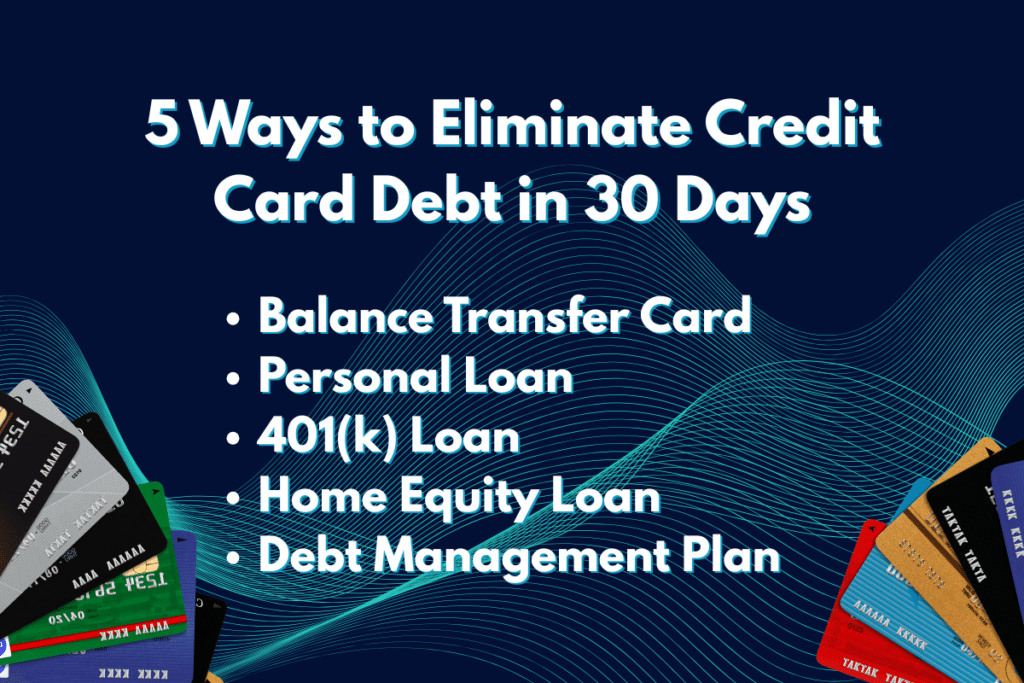

- 5 Ways to Eliminate Credit Card Debt in 30 Days include using a balance transfer card to cut interest, consolidating balances with a personal loan, borrowing strategically from a 401(k), leveraging home equity, or enrolling in a debt management plan to lower rates and simplify payments.

- Balance transfer cards and personal loans work best for fast relief because they immediately reduce high interest, freeing more of your payment to attack the principal.

- Borrowing against assets like a 401(k) or home equity can drastically lower interest costs, but only makes sense with stable income due to serious repayment and collateral risks.

- Debt management plans don’t require new loans and can improve credit over time, but they take longer to set up and are better for long-term stability than quick payoff.

Here are five tested ways to get rid of your credit card debt in 30 days, all without needing to earn another dollar.

Using Balance Transfer Cards

The first way is by getting a balance transfer credit card, which is similar to a balance transfer loan. Say you’ve got a bunch of credit card debt on your current credit card at 25% interest every month, which eats away at your finances. You don’t know what to do. Well, if your FICO score is high enough, you could apply for a balance transfer credit card that transfers your debt from the previous card with 25% interest to a new credit card with 0% interest for the first 12 to 18 months. It usually takes just a few days to set up.

A balance transfer card may be worth it because it’s going to give you a lot of breathing room to tackle credit card debt without being bogged down by interest fees. So, what’s the catch? Firstly, if you don’t have a credit score above 690, it’ll be hard to get approved for a credit card with 0%. If you’re in that 580 to 669 range, you might be able to qualify for a balanced transfer card, but your rate might be closer to 10%, which is better than your current APR. However, keep in mind, these low rates are temporary, just like the 0% interest, and after 6 months to a year, it will shoot back up to the mid-20s.

The second catch is that 0% interest may come with a one time transfer fee of 3% to 5% of the total amount you transfer.1 So, if you’re transferring $10,000 worth of credit card debt, you could be looking at a transfer fee between $3 and $500. But this is still a great option if the transfer fee is less than the interest you would pay over time, which it usually is.

Using Personal Loans

The next way to get rid of credit card debt is to get a personal loan to pay off high credit card balances. This option is a favorite amongst people who are looking to combine a bunch of different debts into just one loan, aka debt consolidation, or if they’re looking to take a high interest credit card debt and trade it for a personal loan with a lower interest rate. Personal loans can be a good option because with debt consolidation, instead of dealing with a bunch of different credit card companies all sending you different letters and written warnings, you can just deal with one company. And that also means you only have to keep track of one bill instead of 10.

Even if your credit score isn’t the best, there are different personal loans out there for all credit score ranges . You can check out creditninja.com to learn about our installment loans or check out the 9,000 plus reviews on Trustpilot. Regardless of what personal loan you end up going with, remember to pay down the debt aggressively. The goal is to eliminate debt, not just transfer it to another account.

Using a 401(k) Loan

The next method for eliminating credit card debt is borrowing against your 401k employer plan. Now, this can be risky, but it might make sense for you if you have an employer sponsored retirement plan, but also have a low credit score.

If your employer’s retirement plan allows it, you can typically borrow up to $50,000 or 50% of your 401k balance, whichever is less.2 There’s no credit check because you’re technically borrowing your own money. That means the interest rate is usually in the single digits instead of 20% or more. Not to mention, instead of paying interest to the loan provider, the interest paid on your 401k loan goes right back to your retirement account. And once you request the loan, it usually takes a few days to a couple of weeks to get the money. You can then use it to pay off your high interest debt in one shot. From there, you start paying the loan back through payroll deductions. And because it comes out of your paycheck automatically, it’s pretty easy to stay on track of repayments.

But that certainly doesn’t mean it’s not without a lot of risk. If you leave your job or get laid off, most 401(k) plans require you to pay back the full balance quickly, sometimes within 60 to 90 days. And if you can’t do that, the IRS may charge income taxes on it and probably a 10% early withdrawal penalty if you’re under 60. So, it’s vital that you have a super stable job if you want to use this method.

Using a Home Equity Loan

A home equity loan gives you a lump sum payment and a HELOC gives you a flexible line of credit. Both offer lower interest rates than credit cards because like the 401k plan, you’re offering something valuable as collateral. In this case, your home. So once again, only consider this option if you’re confident you can handle the payments and you’ve got stable income.

Using a Debt Management Plan

A debt management plan (DMP) could help you get your credit card debt under control without borrowing more money. Here’s how it generally works:

- You talk to a credit counselor. They take a look at everything you owe and then you go to your credit card companies to negotiate lower interest rates for you.

- If the creditors agree, your interest rates drop and your payments get rolled into one monthly payment that you send the agency.

- The credit counselor handles the rest, making sure your credit card companies get paid on time every month.

Enrolling in a DMP doesn’t hurt your credit score. And in many cases, your score starts to go up as your balances go down and your payment history gets back on track. So, it’s a solid option for people who are overwhelmed with minimum payments, need lower interest, but don’t want or can’t qualify for a debt consolidation loan, but it’s probably not the best option if you’re looking for fast results. Because if you contact a nonprofit credit counselor now, it will probably take a few weeks to set up your DMP.

References:

- What is a balance transfer fee and how does it work? │ Credit Karma

- Thinking about a 401(k) withdrawal or loan? │ Principal