Key Takeaways

- Buy now, pay later is increasingly used for everyday purchases, not just large or discretionary items.

- BNPL options increase spending and reduce friction at checkout, benefiting retailers but increasing consumer risk.

- A growing number of users struggle with late payments, overspending, and debt management.

- Missed BNPL payments can lead to high interest, fees, and credit damage.

- Increased regulation signals growing concern about the long-term impact of buy now, pay later on consumers.

Buy now, pay later services have moved far beyond financing large purchases. In 2025, consumers used buy now, pay later options for everyday expenses like food delivery, coffee, clothing, and groceries.2 While this shift may seem convenient, it signals growing financial strain and raises concerns about consumer debt, repayment risk, and long-term financial stability.

Understanding how buy now, pay later works, who uses it, and where it creates risk is essential as these services become more embedded in daily spending.

What Is Buy Now, Pay Later?

Buy now, pay later allows consumers to split a purchase into smaller installment payments, often marketed as interest-free. While installment purchasing has existed for centuries, for example installment loans, modern BNPL platforms have rapidly expanded in recent years.

Today, the global buy now, pay later market facilitates more than $175 billion in purchases, and BNPL options appear on most major online checkout pages.6

Why Buy Now, Pay Later Is Everywhere

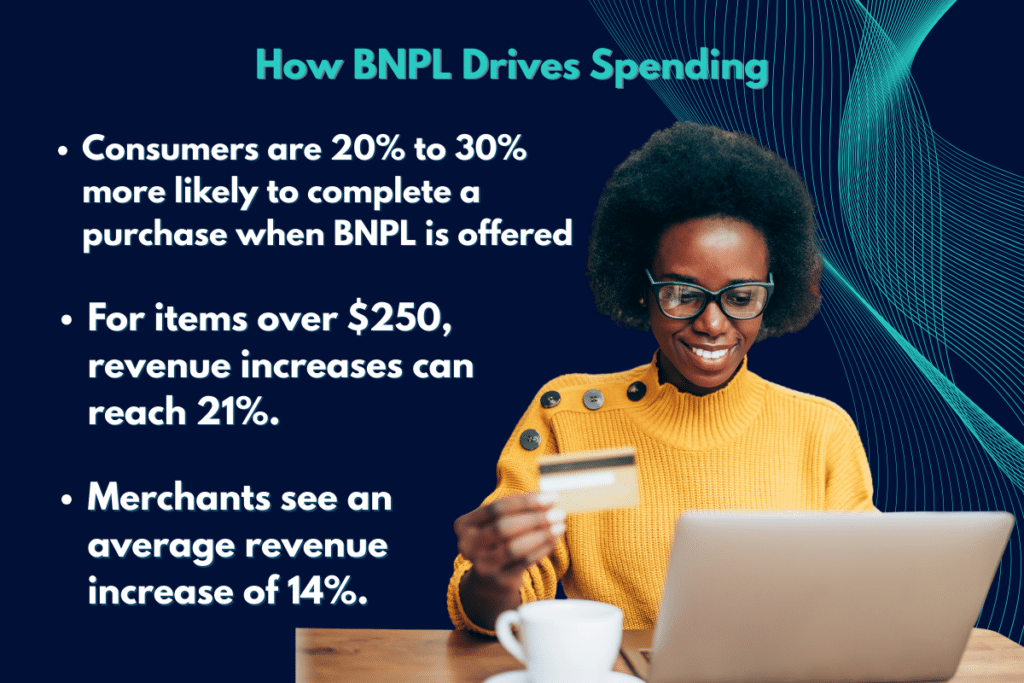

Retailers increasingly offer buy now, pay later because it significantly increases conversion rates.

As a result, BNPL options are now common across:

- Food delivery apps

- Wireless providers

- Major marketplaces like Amazon

- Some credit card companies have also integrated buy now, pay later features directly into their products.

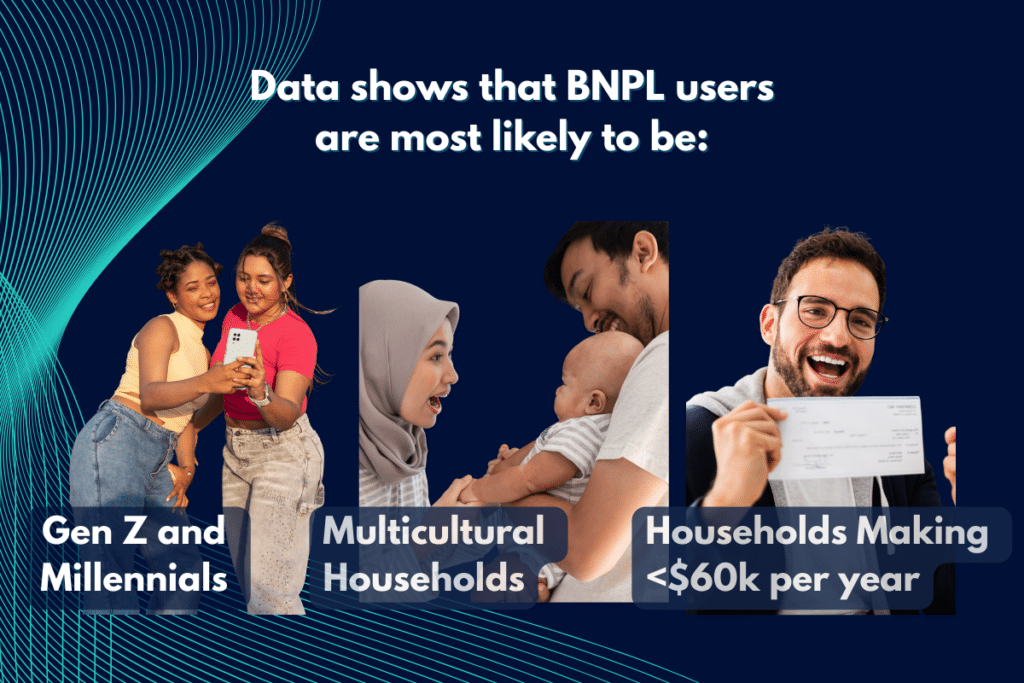

Buy Now, Pay Later Marketing Targets Younger and Lower-Income Consumers

BNPL platforms heavily market their services through social media, digital ads, and pop culture campaigns. This messaging often emphasizes small payments, flexibility, and ease of use while downplaying risk.

Who Uses Buy Now, Pay Later Most

These groups are often more sensitive to cash flow disruptions and more likely to rely on installment payments to manage everyday expenses.

What People Are Buying With Buy Now, Pay Later

BNPL is no longer limited to discretionary or luxury purchases. Here are the most common purchases:

- Clothing and fashion

- Electronics and gadgets

- Furniture

- Home appliances

In addition, a growing number of consumers are using BNPL for:

- Event tickets

- Food delivery

- Groceries and household essentials

Approximately 19% of BNPL users report using these services for groceries and basic household items, a sign that many households are struggling to cover necessities with current income.5

Buy Now, Pay Later and the Rise of Paycheck-to-Paycheck Living

As of 2025, 57% of Americans report living paycheck to paycheck.3 Rising food prices, housing costs, and everyday expenses have made it harder for households to manage cash flow.

For some consumers, splitting small purchases into installments provides short-term flexibility. However, this approach can mask deeper financial problems and increase long-term risk.

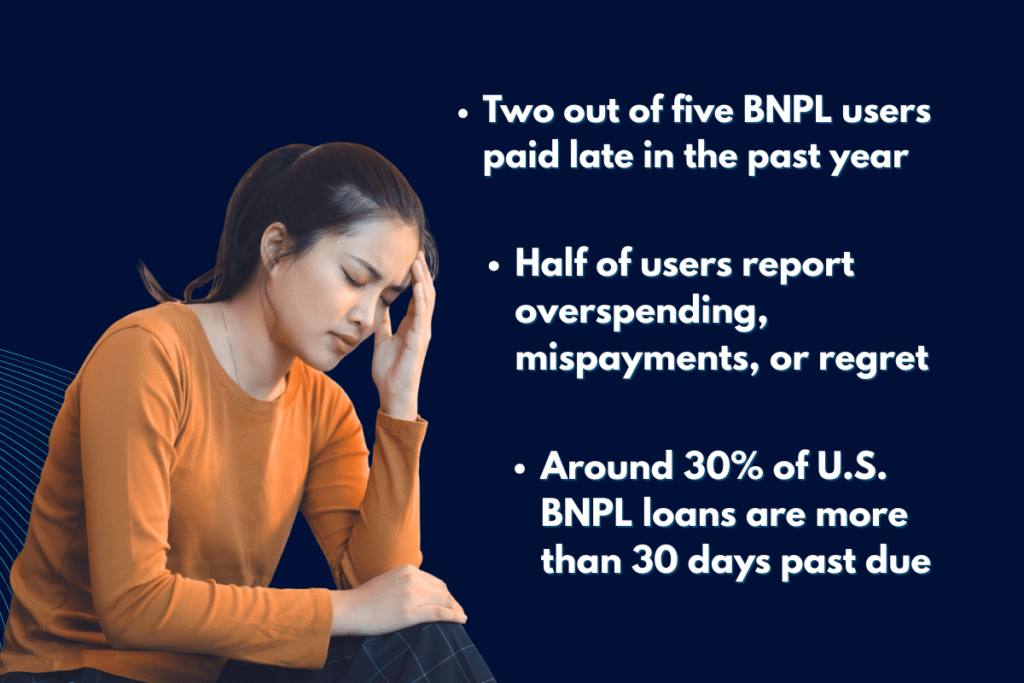

Many Buy Now, Pay Later Users Struggle to Repay

While BNPL is often marketed as low-risk, repayment issues are becoming more common, here are some stats:

These issues suggest that many consumers are using BNPL beyond their ability to repay comfortably. Missing a payment can quickly turn a no-interest plan into high-cost debt.

Potential Costs of Missed Payments

Here are some “hidden” costs of BNPL:

- Interest rates can range from 10% to 36% after missed payments.

- Some BNPL providers charge late fees per missed installment.

- High rates can exceed typical credit card interest.

- In some cases, missed BNPL payments can also negatively impact a consumer’s credit score.

Buy Now, Pay Later Companies Are Also Under Pressure

Despite rapid growth, BNPL providers face significant financial challenges. Klarna, one of the largest BNPL platforms, reported a net loss in early 2025, driven largely by unpaid consumer balances.7

If repayment problems continue, other BNPL providers may face similar financial strain, creating risk for retailers that rely on installment payments to drive sales.

Regulation of Buy Now, Pay Later Is Increasing. Governments are beginning to respond to the risks associated with BNPL. The UK now requires affordability checks for BNPL users. Australia mandates credit licensing and full credit checks starting in mid-2025. U.S. regulators have signaled increased oversight.

These changes suggest that the largely unregulated expansion of BNPL is coming to an end.

Can Buy Now, Pay Later Be Used Responsibly?

Buy now, pay later can be a useful short-term tool if used carefully. However, its ease of access and aggressive marketing make it easy to overborrow.

Consumers who choose to use BNPL should:

- Treat it like a short-term loan.

- Limit the number of active installment plans.

- Stay within a realistic budget.

- Set reminders to avoid missed payments.

Without careful management, BNPL can quickly contribute to debt accumulation and financial stress.

Sources:

- Is BNPL Better for Consumers Than Credit Cards? | Fintechtakes.com

- BNPL headed for credit reports | Axios

- 57% of Americans Live Paycheck to Paycheck in 2025 | Marketwatch.com

- Many Coachella Attendees Are Buying Tickets Through BNPL | Paymentsjournal.com

- Insights Into Buy Now, Pay Later: Growth & Trends 2025 | Numerator

- US BNPL Transactions Hit $175 Billion Amid Shifting Consumer Demands | PYMNTS.com

- Klarna doubles losses in first quarter as IPO remains on hold | CNBC