Key Takeaways

- In 2025, the average American had $7,321 worth of credit card debt.

- Credit card debt continues to rise in 2025, with Millennials and Gen X carrying the largest balances, while younger generations face higher debt relative to income.

- Rising interest rates make carrying credit card balances more expensive, turning manageable debt into high-cost consumer debt if not actively managed.

- High credit card debt impacts credit history and borrowing power, affecting eligibility for personal loans and other financing.

In 2025, the average credit card debt among Americans with unpaid balances is about $7,321, based on data from Q1. The average credit card balance for all credit card holders is roughly $6,371, according to TransUnion and the Federal Reserve Bank of New York.

Meanwhile, the average credit card interest rate on accounts incurring interest has climbed to about 22.25%. Total outstanding credit card debt in the U.S. is now over $1.18-$1.21 trillion, surpassing the national average as reported by the Federal Reserve and related institutions. When compared to monthly income, many Americans are seeing these balances consume a significant portion of their take-home pay.

Understanding the Average Credit Card Debt in America

In 2025, the average credit card APR has risen, turning many balances into high-interest debt. This is pushing households to treat cards like short-term consumer loans, rather than convenient payment tools for emergencies. The average credit card debt among those carrying balances now exceeds prior years, while the average credit card balance for all cardholders remains significant.

As borrowers juggle rates and payments, even modest balances can balloon, and the growing gap between earnings and the average credit card debt highlights why repayment strategies matter more than ever.

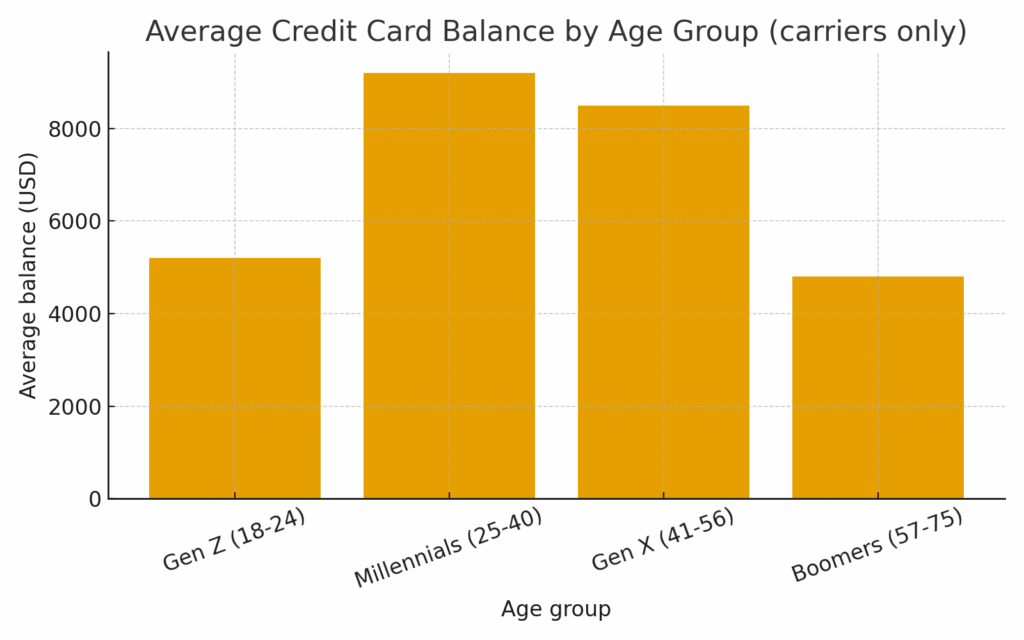

Which Generations Carry the Most Credit Card Debt?

Millennials and Generation X typically carry the largest balances. With a higher-than-ever average credit card APR, those groups feel repayment pressure more acutely, which pushes up the average credit card debt for households in their prime earning years.

Lower-income households may report a lower average credit card balance but face higher debt-to-income strain, and the average credit card debt remains elevated across many demographics.

source: https://www.experian.com/blogs/ask-experian/research/credit-card-debt-by-age/

Age Generation Credit Card Debt at a Glance

Average debt by generation:

- Generation Z (18–27): $3,456

- Millennials (28–43): $6,932

- Generation X (44–59): $9,557

How Does an Interest Rate Impact Debt?

Higher credit card balances accumulate interest faster, turning manageable debt into high-cost consumer debt and putting pressure on monthly budgets.

Even borrowers who pay on time can see their financial flexibility shrink as interest charges grow. Understanding the relationship between credit card debt and broader consumer finances is crucial for making informed decisions about repayment strategies, personal loans, or balance transfers to reduce overall costs.

Credit Card Balances and Debt vs Monthly Income in 2025

Using personal loans or balance transfers can help Americans reduce the cost of high credit card debt caused by rising interest rates. A balance transfer moves existing debt to a lower-interest card, temporarily lowering interest charges and making repayment more manageable. Alternatively, a personal loan can consolidate multiple high-rate balances into a single, fixed monthly payment.

Both approaches give consumers more control over their finances, but it’s essential to account for fees, interest rates, and repayment timelines to ensure the solution truly lowers overall debt.

What Are the Average Credit Card Balance Debt Trends Over Time?

Credit card debt in the U.S. has been steadily increasing over time, with the Federal Reserve Bank reporting that total revolving debt topped $1.2 trillion in early 2025. Rising credit card balances reflect not only higher spending but also the lingering effects of inflation and rising interest rates.

Younger generations are carrying more debt relative to income, while older generations maintain higher absolute balances. Tools like balance transfers remain popular to manage high-interest debt, but balance transfer fees and variable APRs can limit their effectiveness. Monitoring these trends is essential to understanding the evolving landscape of debt and overall consumer finances.

What Are the Risks of Rising Credit Card Balances?

The risks of growing credit card balances can pose problems for personal credit history and long-term financial health. As credit card debt rises, borrowers may face higher interest costs, late payments, and potential over-limit fees, which can damage credit scores. Overreliance on high-interest cards can increase overall debt, making it difficult to qualify for loans or other financing.

While balance transfers can mitigate some risks, balance transfer fees and failure to address underlying spending habits can exacerbate financial strain. Staying proactive about repayment is critical for maintaining strong consumer finances.

Risks at a Glance

- High credit card balances can damage credit history through increased credit utilization and missed payments.

- Rising credit card debt leads to higher interest costs and potential over-limit fees.

- Overreliance on high-interest cards can increase overall consumer debt, limiting access to loans or other financing.

- Balance transfers may reduce interest costs, but balance transfer fees and failure to address spending habits can worsen debt.

- Unchecked debt growth can strain monthly budgets and overall consumer finances, making it harder to save or invest.

Final Thoughts From CreditNinja

In 2025, credit card debt and rising credit card balances continue to challenge Americans’ consumer finances. With interest rates higher than in previous years, managing debt effectively is more important than ever.

Tools like balance transfers and personal loans can help reduce costs, but careful attention to fees, repayment timelines, and credit management is essential. Understanding trends, monitoring balances, and making informed decisions about spending and repayment can help consumers regain control over their financial health and build a strong credit history for the future.

FAQ

How much credit card debt does the average American have?

As of 2025, the average credit card debt for Americans carrying balances is approximately $7,321, though total credit card balances vary by age, income, and spending habits.

How do interest rates affect my credit card debt?

Higher interest rates increase the cost of carrying balances, turning manageable debt into more expensive consumer debt. Even small balances can grow quickly if only minimum payments are made.

Which generation carries the highest average credit card balances?

Millennials (ages 25–40 in 2025) generally carry the highest credit card balances, averaging around $8,200 per cardholder. Gen X (41–56) follows closely with averages near $7,500.

What are balance transfers, and how can they help?

A balance transfer moves debt from a high-interest card to a lower-interest card, temporarily reducing interest charges. However, balance transfer fees apply, and repayment discipline is essential to avoid accumulating more debt.

What trends are driving credit card debt in 2025?

Factors driving credit card debt in 2025 include rising interest rates, inflation, increased spending, and delayed repayments. Younger generations tend to carry debt relative to income, while older groups hold higher absolute balances.

References:

- Average American Credit Card Debt in 2025 | The Motley Fool

- U.S. Average Credit Card Debt In 2025 | Forbes Advisor

- Consumer Credit | Federal Reserve

- Income in the United States 2024 | Census.gov

- Average Credit Card Debt by Age in 2025 | Experian

- Growth Remains Steady; Auto Loan Originations Pick Up | Federal Reserve Bank of New York

- What to do if your credit score has dropped | AP News