Key Takeaways

- About 41% of Americans—roughly 72 million people—have medical debt or are struggling with medical bills.

- Medical debt estimates vary widely because surveys capture all types of debt while credit reports only show accounts sent to collections.

- Lower-income households, Black and Hispanic adults, uninsured or underinsured individuals, and adults aged 50–64 are the most likely to carry medical debt.

- Most medical debt balances are under $500, but millions of Americans owe $10,000 or more, often due to major medical events or chronic conditions.

Approximately 72 million people (41% of working-age Americans) have medical bill problems or are currently paying off medical debt, according to a survey from The Commonwealth Fund.

Medical debt is often used as an umbrella term for all health care debt, including medical or dental bills, and other debt accruing from health care bills (e.g., payment plans, credit cards, bank loans, and borrowing from family and friends).

The percentage of medical debt varies considerably based on the survey size and source. Some surveys capture all debt types for more people, while credit reports only show debt sold to collectors, and collections data misses debt paid directly or still in dispute. In addition, recent credit bureau changes (such as removing sub-$500 debts) have significantly reduced those numbers, leading to higher survey counts and lower credit report/collections counts for the same underlying issues.

How Is Health Care Debt Measured?

Health care debt is measured using surveys, credit bureau data, and provider data. Various organizations—including federal agencies, nonprofit research groups, credit bureaus, financial technology companies, healthcare providers, and media outlets—collect different forms of medical debt data.

- Household Surveys — Surveys ask people whether they owe money for medical or dental care, including payment plans, credit card balances, loans, or bills not yet in collections.

- Credit Bureau Data — Credit bureaus track medical debt only when it goes to collections and appears as a derogatory mark on a credit report.

- Provider/Hospital Billing Data — Researchers analyze what hospitals classify as “bad debt” or uncompensated care, typically bills patients were expected to pay but did not.

Pros And Cons of Measurement Methods

These are some of the pros and cons of different measurement methods used to track medical debt:

Household Surveys

Pros

- Captures Hidden Debt – Such as unpaid bills, loans from family, credit card debt used for medical expenses.

- Provides Demographics – Allows analysis by income, race, insurance type, age, etc.

- Affordable – Relatively cost-effective to collect.

Cons

- Self-Report Bias – People may not remember exact amounts or may under/over-report.

- Not Real-Time – Surveys often reflect conditions months or years earlier.

- Terminology – Different survey wording leads to inconsistent results.

Credit Bureau Data

Pros

- Large-Scale, Objective Data – Millions of records reflect national trends.

- Useful For Policy Analysis – E.g., after credit-reporting rule changes (like removal of paid medical collections).

Cons

- Only Captures Debt In Collections – Ignores payment plans, charity care, unpaid bills not yet sent to collections.

- Policy Changes Distort Trends – Recent rules (2022–2023) removed much medical debt from credit reports, limiting comparability over time.

- No Demographic Detail – You can’t easily tell who holds the debt.

Provider/Hospital Billing Data

Pros

- Highly Detailed Billing Information – Shows what services cost and what went unpaid. Useful for estimating the burden on hospitals and systems.

Cons

- Does Not Represent Patient Experience – Includes charges patients never intended to pay or could not understand.

- Limited Scope – Each system provides only its own data; not nationally standardized.

- Overstate Debt – May overstate debt because charges often exceed negotiated or final bill amounts.

Who Is Calculating Health Care Costs?

Multiple organizations track medical debt in the United States, but their estimates differ because they measure different types of debt, use different data sources, and define “medical debt” in distinct ways.

The Kaiser Family Foundation, Urban Institute, and Consumer Financial Protection Bureau are the three major sources for medical debt data, and these are their most recent findings.

Kaiser Family Foundation (KFF)

The Kaiser Family Foundation (KFF) national surveys show that about 41% of U.S. adults currently have some form of medical or dental debt. This includes any unpaid medical bill, whether it’s on a credit card, in a payment plan, owed to family, or waiting to be sent to collections. Because the definition of medical debt is broad, the percentage is the highest among major estimates.

Urban Institute

The Urban Institute estimates that around 36% of households owe medical debt. Their method relies on household financial surveys and modeling to capture balances owed for medical services, including those not reported to credit bureaus.

CFPB (Consumer Financial Protection Bureau)

CFPB, which analyzes data from the three major credit bureaus, reports that roughly 15 million Americans have medical debt on their credit reports.

Because credit reports only show medical bills that have gone to collections, and recent rule changes removed many medical collection accounts under $500 or paid in full, this figure is much lower than survey-based estimates.

Who Is Most Affected By The Burden of Medical Debt?

Medical debt can hit almost anyone, but it doesn’t hit everyone evenly. Some groups are much more likely to carry unpaid medical or dental bills than others, especially when income, race, health insurance coverage, and age are factored in. Recent analyses from KFF, the Urban Institute, and federal survey data highlight who is most at risk.

| Group | Approx. share with medical debt |

| All U.S. adults (broad KFF definition) | ~41% have medical or dental debt |

| Black adults | ~56% report unpaid medical/dental bills (broad survey); ~13% with significant debt (SIPP) |

| Hispanic adults | Higher than White adults (exact share varies by survey, but consistently elevated) |

| White adults | ~37% report unpaid medical/dental bills (broad survey); ~8% with significant debt (SIPP) |

| Lower-income households | Roughly 1 in 10 adults below 400% of the poverty line report significant unpaid medical bills |

| Part-year uninsured adults | ~14% report significant medical debt (vs. 8% fully insured) |

| Adults 50–64 | ~10% report significant medical debt |

| Adults 65–79 | ~6% report significant medical debt |

Illustrative example using recent KFF and Peterson–KFF analyses of adults with “significant” medical debt (generally >$250 in unpaid medical bills).

Low-Income Households Carry Disproportionate Debt

People with lower incomes are far more likely to end up with medical debt than higher-income households. KFF’s analysis of federal SIPP data finds that about 1 in 10 adults with incomes below 400% of the federal poverty level are more likely to report significant unpaid medical bills than higher-income adults. Even relatively small unexpected bills can be unaffordable for lower-income families, especially when they have limited savings or unstable employment.

Higher Percentages Among Black And Hispanic Adults

Medical debt can reflect deep racial and ethnic unfairness, take a look at some stats:

- KFF’s broad health care debt survey finds that Black and Hispanic adults are more likely than White adults to report having health-care–related debt, even after accounting for insurance status.

- A KFF/NPR “Diagnosis: Debt” investigation found that about 56% of Black adults reported owing money for a medical or dental bill, compared with 37% of White adults.

- In SIPP-based data, 13% of Black Americans report significant medical debt, compared with 8% of White Americans and 3% of Asian Americans.

These gaps reflect not just differences in health status and insurance, but also long-standing disparities in income, wealth, and treatment within the health system.

Higher Debt Among Uninsured or Underinsured Groups

Health insurance coverage matters, but having insurance doesn’t fully shield people from debt.

- KFF’s SIPP analysis shows that adults who went without health insurance for part of the year are most likely to report medical debt (about 14%), compared with 8% of those insured all year and 11% of those uninsured the entire year.

- KFF’s broader survey finds that uninsured adults and those with high deductible health plans are among the most likely to owe medical debt, even when they technically have coverage.

As you can see, both gaps in coverage and underinsurance (high deductibles, coinsurance, and surprise bills) drive people into debt.

Age-Related Differences

Age also ties into carrying medical debt. Unfortunately, medical debt tends to build during working-age years, but remains a problem for some older adults who face coverage gaps or high out-of-pocket costs.

- Adults in midlife tend to carry the most medical debt. KFF’s SIPP analysis shows that 10% of adults ages 50–64 report significant medical debt, compared with 6% of adults ages 65–79, who are more likely to have Medicare.

- Younger adults may have lower average medical spending, but they’re also more likely to lack savings or stable insurance, which can make even smaller bills problematic.

How Much Do Americans Owe?

The average American’s medical debt varies by report, but recent data shows an average of over $3,100 on credit reports for those with collections and a median of $2,000 for all debt. Medical bills range from small, one-time bills to large balances that can negatively impact households for years.

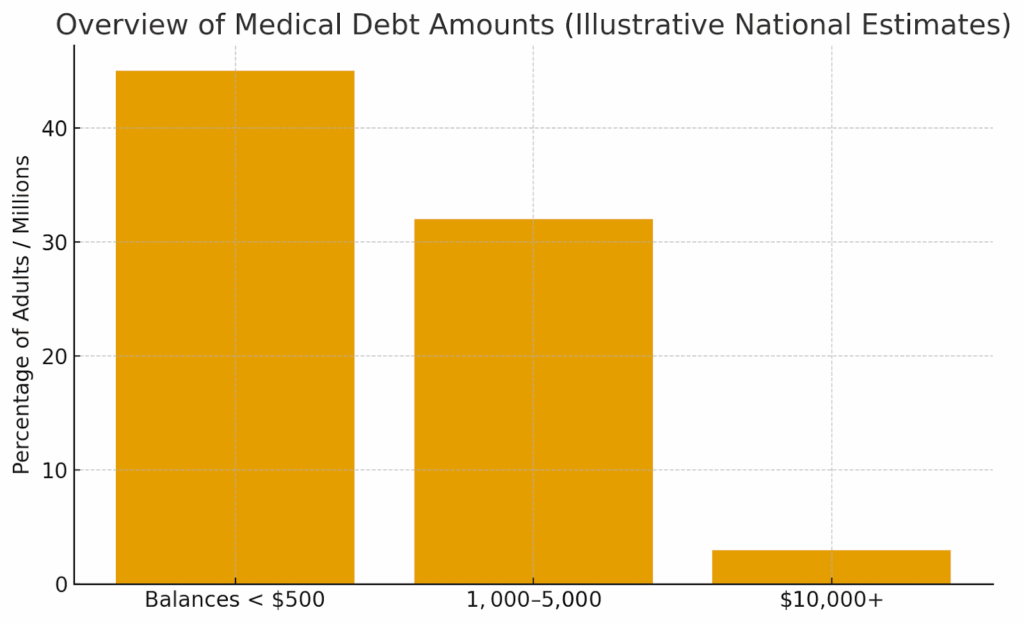

Here’s a visual chart that displays an overview of medical debt amounts:

As you can see, the majority of Americans have less than $500 in unpaid health care costs. But the reason for owing money directly affects the amount a person carries.

- Small Balances (<$500): Approximately 45% of adults with medical debt owe less than $500. These small balances often come from outpatient visits, urgent care, or unexpected copays.

- Moderate Balances ($1,000–$5,000): Around 32% of debt holders owe between $1,000 and $5,000. This range often represents surgical procedures, diagnostic testing, ER visits, or costs associated with high-deductible health plans.

- High Balances ($10,000+): Roughly 3% of adults with medical debt owe more than $10,000. These large debts are typically tied to major hospitalizations, chronic conditions, or extended medical treatment.

What Can You Do if You Have Medical Debt?

If you have outstanding medical debt,it’s important to work on paying it off. Unpaid medical bills can affect your credit, be sent to debt collection agencies, or result in lawsuits for wage garnishments.

Here are 5 effective debt repayment strategies you can use to cut down on

| Strategy | What It Means | Steps to Take |

| Disputing Billing Errors | Correcting charges that are inaccurate, duplicated, or not performed. | 1. Request an itemized bill. 2. Highlight unfamiliar or duplicate codes. 3. Call the provider’s billing department to dispute errors. 4. Ask for a corrected bill in writing. 5. If unresolved, file a written dispute and escalate to your insurer or state insurance regulator. |

| Checking Credit Scores | Ensuring medical debt is reported accurately—or not reported when it shouldn’t be. | 1. Pull free credit reports at AnnualCreditReport.com. 2. Look for medical collections that are incorrect, paid, or under $500 (which should be removed under new rules). 3. Dispute inaccurate entries with the credit bureau online or by mail. 4. Monitor credit monthly to confirm updates. |

| Requesting Itemized Bills | Getting a detailed breakdown of all charges to understand what you owe. | 1. Call the provider and ask for an itemized, CPT-coded bill. 2. Review line items for duplicate charges, services not received, or coding errors. 3. Compare against your Explanation of Benefits (EOB). 4. Dispute discrepancies before paying. |

| Getting Financial Assistance | Applying for help from hospitals or nonprofits to reduce or eliminate bills. | 1. Ask the provider about their charity care or financial assistance program (nonprofit hospitals are legally required to offer one). 2. Complete the application with income documentation. 3. Request a temporary hold on collections while your application is processed. 4. Receive approval/denial and request clarification if needed. |

| Setting Up Payment Plans | Negotiating a monthly repayment schedule you can afford. | 1. Contact the provider or collections agency to request a plan. 2. Ask for 0% interest if possible (many providers offer this). 3. Choose a monthly amount that fits your budget. 4. Get the agreement in writing and set up automatic payments. 5. If terms are too high, negotiate again or seek financial assistance first. |

How Does Medical Debt Affect Your Credit?

Medical debt affects your credit if you owe more than $500. Amounts less than $500 no longer appear on credit reports. However, larger unpaid medical bills can hurt your credit score if the debt is sold to a collection agency. Debt sold to collections can significantly damage your score for up to seven years. This can make it harder for you to qualify for loans, housing, and insurance. Carrying high amounts of medical debt can also negatively affect health due to higher rates of anxiety, stress, and depression.

FAQ

What percentage of Americans have medical debt?

According to a survey from The Commonwealth Fund, about 72 million people have medical medical debt. That’s about 41% of working-age Americans.

Why do different sources report different percentages?

Different sources report different percentages due to differences in what they measure (credit reports vs. surveys), who they survey, how they define debt, and data limitations.

Does medical debt still affect your credit score?

Medical debt can negatively affect your credit if it’s sold to a debt collection agency. Collection accounts can continue to affect your credit for up to seven years from the date it’s added.

What is considered a “high” amount of medical debt?

The definition of a “high” amount varies, but generally, medical debt is high if it’s over 20% of your annual income. Medical debt is especially high when it affects a household’s finances and their ability to afford basic necessities. If you have high debt, you can use debt repayment strategies, such as setting up payment plans with the healthcare provider or getting financial assistance from nonprofit organizations.

References:

- 79 Million Americans Have Problems with Medical Bills │The Commonwealth Fund

- The Broad Consequences Of Medical And Dental Bills│KFF

- Health Care Costs and Affordability│KFF

- Why Black Americans are more likely to be saddled with medical debt│NPR

- The burden of medical debt in the United States│Health System Tracker

- Americans’ Challenges with Health Care Costs│KFF