Having less than $5,000 in savings can place you in a financially vulnerable position. Without a sufficient financial cushion, even a relatively small unexpected expense, such as a car repair or medical bill, can lead to debt or long-term financial instability.

The good news is that improving your financial situation does not require complex strategies or drastic lifestyle changes. With a structured approach and consistent effort, it is possible to build stability, reduce financial stress, and work toward long-term security.

Below is a four-step plan designed to help you regain control of your finances and start building a stronger foundation.

Why Taking Action Now Is Important

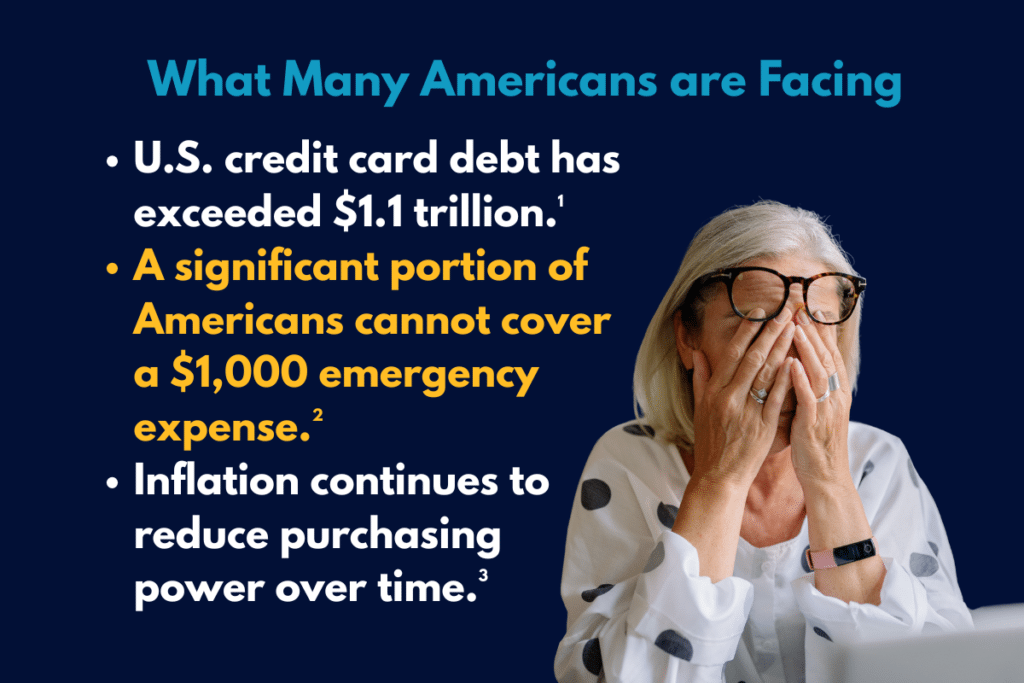

Current financial trends highlight the urgency of building savings and improving financial habits. Many Americans are facing increased financial pressure due to rising costs and growing reliance on credit.

Without proactive financial planning, it becomes increasingly difficult to keep up with rising expenses and avoid long-term financial strain. Taking action early can help prevent small financial challenges from becoming larger problems.

Step 1: Build an Emergency Fund

An emergency fund is a critical component of financial stability. It should be kept separate from your everyday spending accounts and reserved strictly for unexpected expenses.

Unplanned costs, such as medical emergencies, home repairs, or job disruptions, are one of the most common reasons individuals fall into debt. Having a dedicated emergency fund helps reduce reliance on credit during these situations.

How to Get Started

To begin building an emergency fund, it is important to understand your current financial situation:

- Calculate your total monthly income

- Track your monthly expenses

- Identify areas of non-essential spending that can be reduced

The money saved from cutting unnecessary expenses should be redirected into a dedicated savings account.

Where to Store It

A high-yield savings account (HYSA) is often recommended because it offers higher interest rates than traditional savings accounts. Many HYSAs currently offer returns in the range of 3–5%, which can help your savings grow over time while maintaining liquidity.

Target Goal

The general recommendation is to save three to six months’ worth of living expenses. This provides a sufficient buffer to handle most unexpected financial situations.

Step 2: Eliminate High-Interest Debt

High-interest debt, particularly credit card debt, is one of the most significant barriers to financial progress. With average credit card interest rates exceeding 20%⁴, balances can grow quickly if they are not aggressively managed.

When only minimum payments are made, a large portion of the payment may go toward interest rather than reducing the principal balance. This can significantly extend the time required to pay off the debt.

Recommended Strategies

- Pay more than the minimum payment whenever possible

- Focus on paying off the highest-interest balances first (debt avalanche method)

- Avoid taking on additional debt unless absolutely necessary

Eliminating high-interest debt should generally take priority over investing, as the cost of interest often outweighs potential investment returns.

Step 3: Increase Your Income

While reducing expenses is an important step, it has natural limits. Increasing your income can significantly accelerate both savings growth and debt repayment.

Common Approaches

- Taking on a side hustle, which can generate additional monthly income

- Applying for higher-paying roles or seeking promotions

- Developing new skills to improve earning potential

Even relatively modest increases in income can have a meaningful impact over time, particularly when that income is consistently directed toward savings and debt reduction.

Step 4: Begin Investing After Building Stability

Investing is an important step in building long-term wealth, but it should only be pursued after achieving financial stability. This includes eliminating high-interest debt and establishing a fully funded emergency account.

Historically, diversified stock market index funds have produced average annual returns of approximately 8–10% over the long term⁵. While these returns are not guaranteed, they illustrate the potential of consistent investing.

Long-Term Impact

Regular contributions—such as investing $500 per month—can grow significantly over time due to compound interest. The earlier and more consistently you invest, the greater the potential for long-term growth.

Getting Started

- Open a retirement account, such as a Roth IRA, or a brokerage account

- Invest consistently in diversified index funds

- Focus on long-term growth rather than short-term market fluctuations

Avoid Lifestyle Inflation

One common mistake individuals make after improving their financial situation is increasing their spending. This is often referred to as lifestyle inflation.

While it may be tempting to upgrade your lifestyle as your income increases, doing so can slow or even reverse financial progress. Maintaining disciplined spending habits is essential for achieving long-term financial goals.

Final Thoughts

Having less than $5,000 in savings should be viewed as a signal to take action rather than a permanent limitation. With the right strategy and consistent effort, it is possible to improve your financial position over time.

A structured approach can help you regain control:

- Build an emergency fund

- Eliminate high-interest debt

- Increase your income

- Invest consistently for long-term growth

By focusing on these steps and maintaining disciplined financial habits, you can create a more secure and stable financial future.

Check out more financial topics like, 6 best personal loans for bad credit (2026 guide), at the CreditNinja blog!

References

- Household Debt and Credit Report | Federal Reserve Bank of New York

- Economic Well-Being of U.S. Households | Federal Reserve

- Consumer Price Index (CPI) | U.S. Bureau of Labor Statistics

- Consumer Credit Report | Federal Reserve

- Consumer Expenditure Survey | U.S. Bureau of Labor Statistics